How to Roll Cash-Secured Puts (and when to take assignment)

The stock has dropped. Your short put is at or near the money. The decision in front of you depends almost entirely on a question that gets skipped too often — would you actually mind owning the shares at this strike?

If you ended up here, the situation is probably specific. You sold a cash-secured put a couple of weeks ago at a strike that felt comfortable. The stock has weakened. The put is now worth more than you sold it for, your delta has climbed past 0.40, and you are starting to think about whether to roll, close, or take the shares.

The right move depends less on what the put is doing and more on why you sold it in the first place. A cash-secured put sold as a wheel entry — at a strike you are content to own the stock at — calls for a different response than a put sold purely for premium income on a name you have no interest in holding. This article walks through the framework either way: the trigger signals, the four real options on each side of that fork, the Greeks behind the decision, a worked ABBV example, the trap that catches most premium sellers, and a flowchart to anchor it.

What a cash-secured put actually is

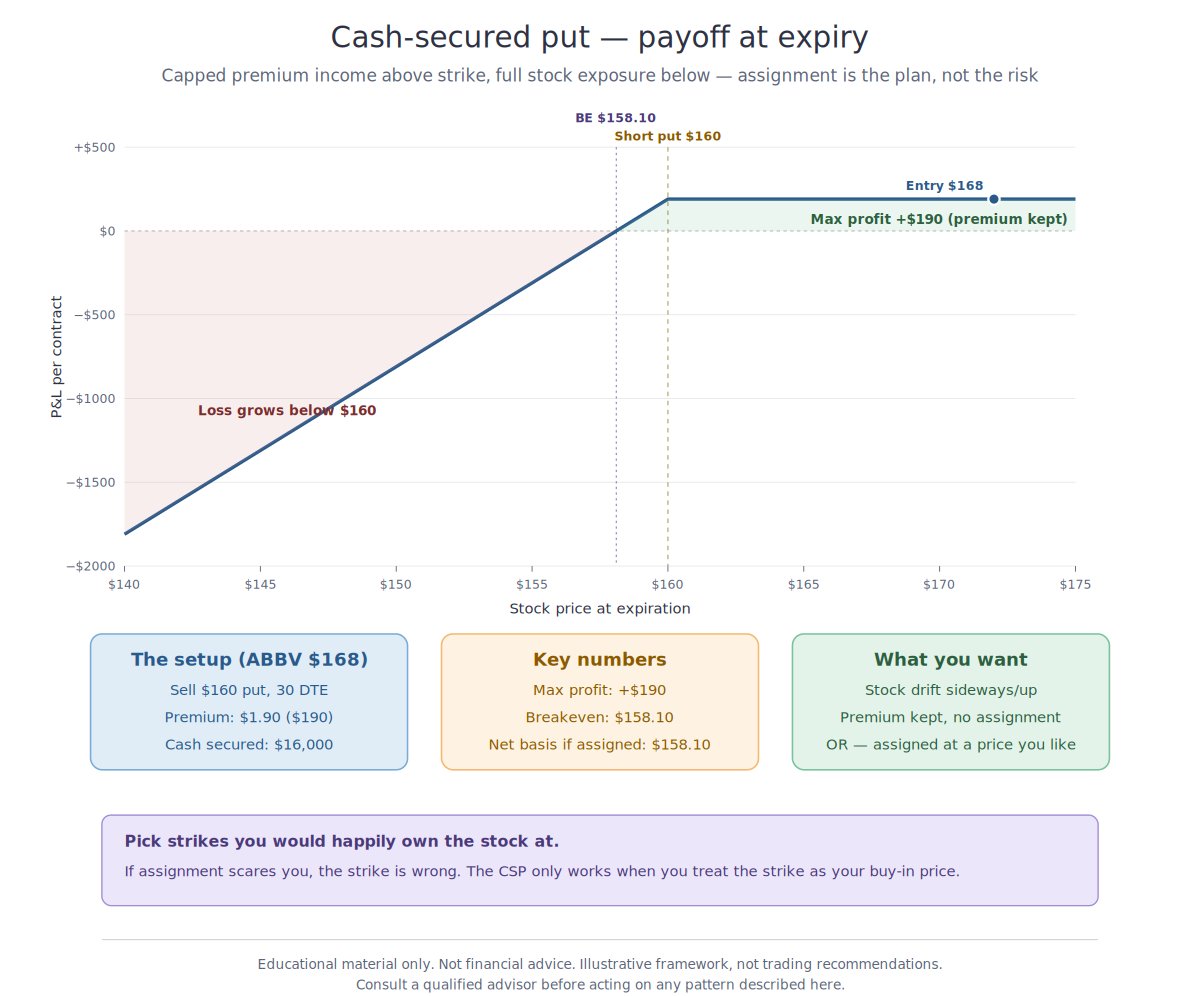

A cash-secured put is a position where you hold cash equal to 100 shares × strike price and sell a put against it. The premium is collected up front and is yours to keep no matter what. If the stock stays above the strike, the put expires worthless — you keep the cash and the premium and move on to the next cycle. If the stock closes below the strike at expiry, the position is assigned: the cash buys 100 shares at the strike, with the premium effectively discounting your cost basis.

The payoff at expiry has the same shape as a covered call — capped income above the strike, full stock-style exposure below it. Mechanically a cash-secured put is a synthetic covered call: same risk profile, same payoff diagram, same considerations.

When the adjustment conversation typically starts

The stock has dropped and the short put is now in or near the money. Two scenarios show up most often, and which one you are in shapes the entire adjustment conversation.

Scenario 1 — assignment is an acceptable outcome. The put was sold as a wheel entry. You picked the strike at a price you were content to own the stock at. Assignment in this context is a designed outcome, possibly the goal.

Scenario 2 — assignment is no longer an acceptable outcome. The put was sold primarily for premium income, and circumstances have shifted. The chart broke, the fundamentals changed, or the original thesis no longer holds. Assignment now would leave you with stock you do not want to own.

Trigger signals

- Delta on the short put has moved from 0.20–0.35 at entry toward 0.45+. The market is now pricing assignment as more likely than not.

- DTE has dropped inside 21 with the stock at or below the strike. Gamma is accelerating — the position becomes faster-moving from this point forward.

- The stock has broken a key technical level — support, the 200-day moving average — that was part of the original entry thesis.

- A negative fundamental event has landed — earnings miss, guidance cut, regulatory news, sector downgrade — and the original reason for selling the put no longer applies.

- Broad market is selling off and the stock is moving with it, not for anything company-specific. A harder signal to read cleanly — the pressure may pass, or it may be the start of a longer downtrend.

Three options when assignment is acceptable

If the strike was chosen at a price you would happily own the stock at, the question is no longer "how do I avoid assignment?" — it is "is assignment now, or some version of buying time, the better path?"

A — Accept assignment

When the strike was chosen as a price you were content to pay, you can simply allow the put to expire ITM. The shares are acquired at a net cost of strike minus premium collected. This is what the wheel was designed to do. It is one of the most overlooked options on the playbook because it feels passive — but it is the trade working as planned.

B — Roll down and out for a credit

The current put is closed and a new put is opened at a lower strike and later expiry. The transaction reduces assignment risk while extending duration. One rule matters more than any other: accept the trade only if it collects a net credit. And one piece of practitioner judgment matters almost as much: limit yourself to a single roll on a given position. Each additional roll tends to compound capital exposure rather than resolve it.

C — Roll down and out for a debit (rare)

Same mechanics as B but with a net debit outlay. This one is rare for a reason — extending a losing position without improving the compensation rarely improves the outcome. A small minority of traders consider it when the strike reduction is dramatic ($5+ lower) and the extended duration gives a realistic chance of recovery. Most do not.

Three options when assignment is no longer acceptable

If the original thesis has broken, the calculation flips. Holding to expiry now means accepting shares of something you no longer want. The available paths look very different.

A — Close the put at a loss

Buy the put back for more than you sold it. This is the cleanest exit when the thesis has broken — a defined, capped loss in exchange for freeing the cash collateral, with no stock entering the account. Paying $2.00 to close a put sold for $1.20 is unpleasant, but it is a known $80 loss per contract rather than potentially holding 100 shares of a name that is no longer on the want-list.

B — Roll to a much lower strike, accept smaller or no credit

Worth considering when some belief in eventual recovery remains but assignment risk needs to be sharply reduced. The strike moves 5–10% below the current stock price. The premium collected tends to be small — that reduction is the trade-off for dramatically reducing assignment probability.

C — Close the put and take a bearish position instead

If your view has flipped from neutral-to-bullish to actively bearish, you can close the short put and consider a put debit spread or long put on the same underlying. This is a thesis change, not an adjustment — and the position size typically changes to match the new conviction and risk profile.

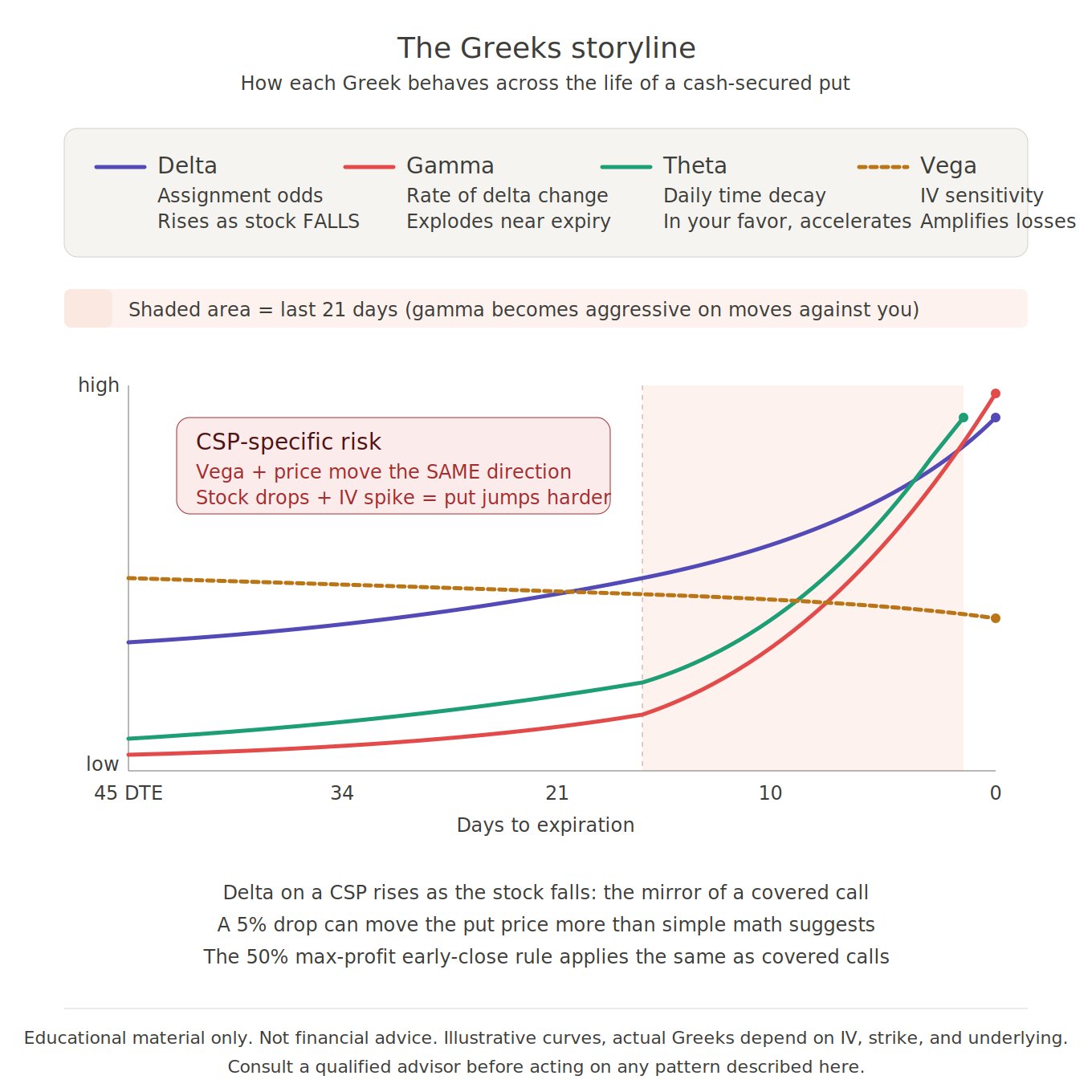

The Greeks behind the decision

The options above are the what. The Greeks explain the when — why the same position can be easy to manage at 35 DTE and nearly impossible at 7 DTE, and why a 5% drop in the stock can move the put more than the math would suggest.

Delta — the mirror of a covered call, running the other way. Entry for a typical CSP is around 0.30 delta — roughly a 70% chance the put expires worthless. CSP delta rises as the stock falls, which is the opposite of a covered call. When delta climbs to 0.45–0.60, the stock has moved meaningfully against the position and assignment is now the more likely outcome. Past 0.70, the short put starts behaving almost like being long 100 shares — every dollar the stock drops costs the position nearly dollar-for-dollar. Of all the Greeks, this is the one to watch first.

Gamma — quiet early, urgent late. At 45 DTE with the stock well above the strike, gamma is low and the position is stable. Under 21 DTE with the stock near or below the strike, gamma turns aggressive — delta can swing 0.15–0.20 on a single 3% stock move. For a trader holding the put as a premium-only trade with no interest in the underlying, last-three-week gamma is what turns "this will probably be fine" into "assignment next Friday" inside two trading sessions.

Theta — the paycheck, and it never stops paying. Theta accrues in the position's favor every single day. It accelerates in the last 21 days and peaks in the final week. The 50% max-profit early-close principle applies the same as for covered calls — it captures most of the theta reward while stepping aside before gamma becomes difficult to manage. On a CSP where assignment is no longer acceptable, closing at 50% max profit also removes the last-week scenario where the stock gaps below the strike on a headline.

Vega — small, running the wrong way, and bigger on high-IV names. A short put position is short vega — rising IV raises the price of the put, which raises the cost to close the position. The common failure mode: a put is sold on a stable stock at low IV, the stock drops 4% on sector news, and IV jumps 10 points at the same time. The put is now 40% more expensive than simple price-movement math would suggest — part of the excess from the stock move, part from the IV repricing. Puts sold into already-high IV on names that would be unwanted at the lower strike have produced some of the more painful adjustment situations on record. The entry premium looks rich — the exit math gets brutal if the stock moves.

The interaction that matters. When a stock starts breaking down, three things tend to happen at once: delta rises as the stock approaches the strike, gamma is already high because DTE is under 21, and IV spikes because the market is pricing more downside. All three work against a short put simultaneously. A put sold for $1.20 can be quoted at $3.50 after a 5% stock drop, not $2.50 — the excess comes from vega expansion. The pattern is consistent: the stock began weakening several sessions before the put price exploded. Closing while the math is still forgiving has been more survivable than managing through the full setup.

The Greeks in plain English

The five paragraphs above use the names traders give to five different ways a cash-secured put can move — delta, gamma, theta, vega, and how they combine. In plainer terms:

Delta is the current odds the put ends up assigned. Low is typically desired (around 25–30% at entry), and 45% is where the position usually warrants a fresh look.

Gamma is how fast those odds change when the stock moves. Low and manageable early, aggressive in the last three weeks.

Theta is the daily income from time passing — which is why the trade pays at all. It speeds up near expiration, but so do the risks. Closing at roughly half the maximum profit is a common rule of thumb for that reason: take most of the reward, skip the messy part.

Vega is the penalty that appears when market-wide fear rises — earnings week, macro headlines, broad selloffs. For a CSP, vega and price movement almost always push in the same direction, which is why a 5% stock drop can send the put's price up by more than the math would suggest.

The "interaction" paragraph is describing a specific bad setup for a CSP trader who does not want the shares: the stock starting to weaken AND DTE under three weeks AND IV expanding, all at once. Most traders who learn to recognize that setup find it easier to exit before it fully arrives than to manage it afterward.

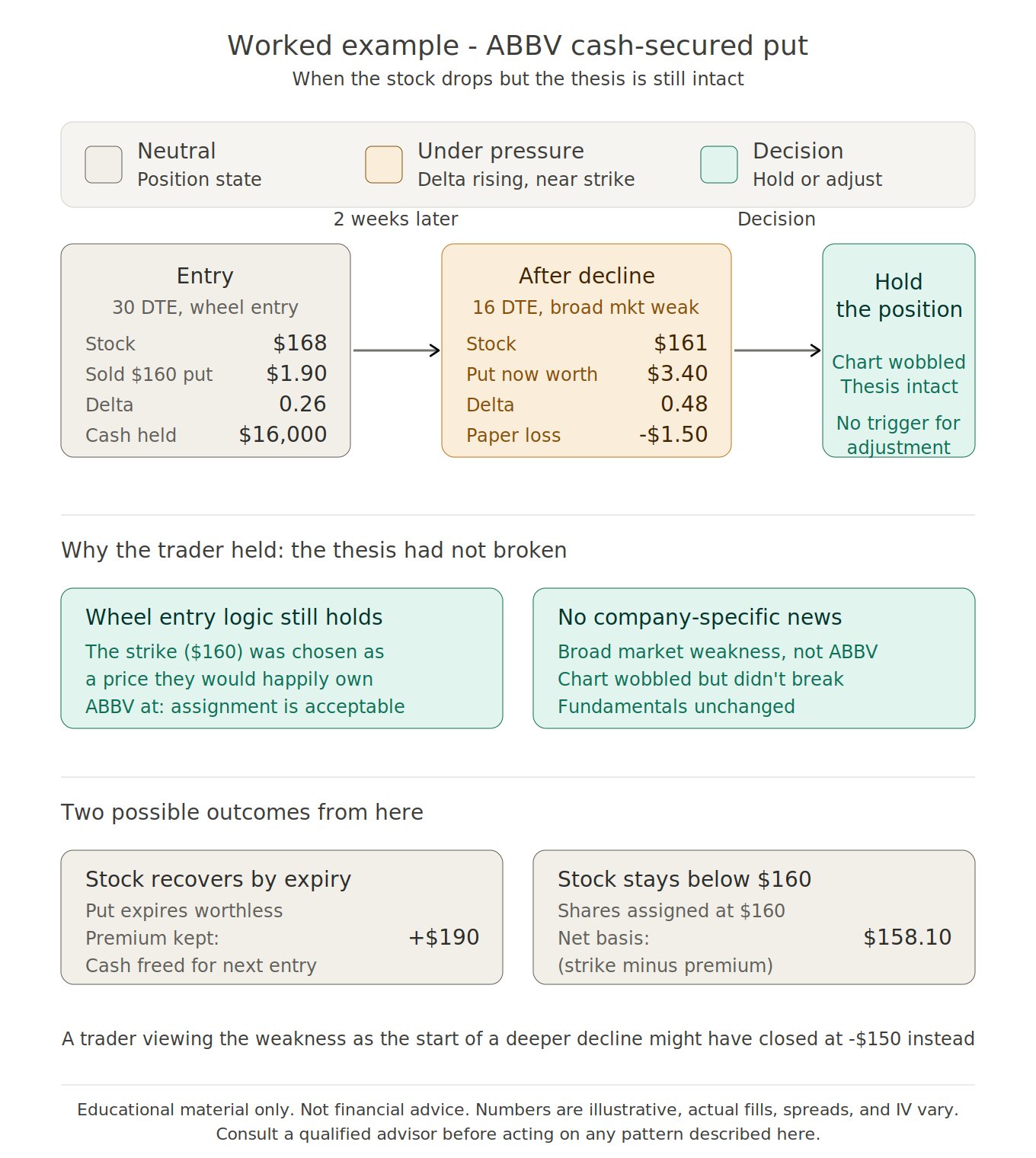

A worked example: ABBV

Setup. ABBV trading at $168. A trader holds $16,000 in cash and sells the $160 put for $1.90 with 30 DTE. Entry delta approximately 0.26. The trader is content to own ABBV at $160 if assigned — this is a wheel entry, not a pure premium trade.

What happened. Two weeks later ABBV is at $161. The short put is now worth $3.40, which represents a $1.50 unrealized loss. Delta on the short put is 0.48, DTE is 16. No company-specific news — just broad market weakness over the period.

One potential response. The thesis remained intact. The stock was near the strike but had not broken — no negative fundamental event, no broken support level, just a weak couple of weeks for the broader market. The position was held into expiry as designed. In the assignment case, the net basis would be $160 − $1.90 = $158.10 per share. In the non-assignment case, the position pays back as theta finishes. The roll button was not used because the trigger signals had not confirmed a thesis change — only the chart wobbled, not the reasoning behind the entry.

This is one path among several. A trader who viewed the broad-market weakness as the start of a deeper decline might have closed the put at the $1.50 paper loss instead and redeployed the capital elsewhere. A trader running this purely for premium with no interest in owning ABBV would have closed earlier — well before delta got to 0.48. The decision is shaped by the original reason for the trade, not by the screen at any given moment.

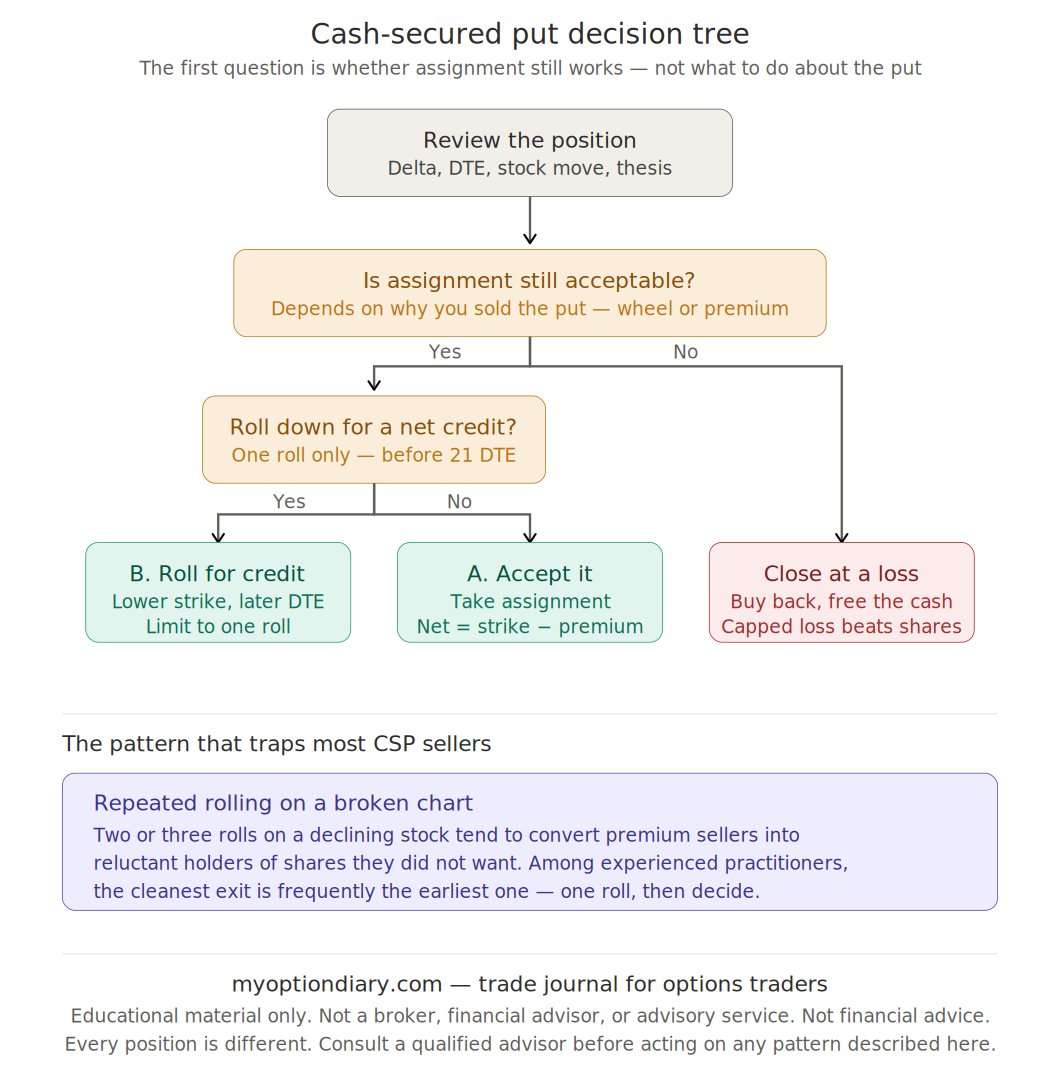

A decision tree to anchor the choice

When the position is moving and the screen is asking for a decision, the actual question to answer is rarely "should I roll?" It starts further back: is assignment still acceptable? If yes, the path forks toward holding or rolling for a credit. If no, the path forks toward closing or repositioning. The flowchart below traces those questions in roughly the order they need to be asked.

The principle worth tattooing somewhere: the cleanest exit is frequently the earliest one. A position that is starting to drift can usually be managed for a small known loss. A position that has been rolled three times on a declining stock is much harder to exit cleanly, and the longer the chain gets, the more often it ends with shares of something you did not want.

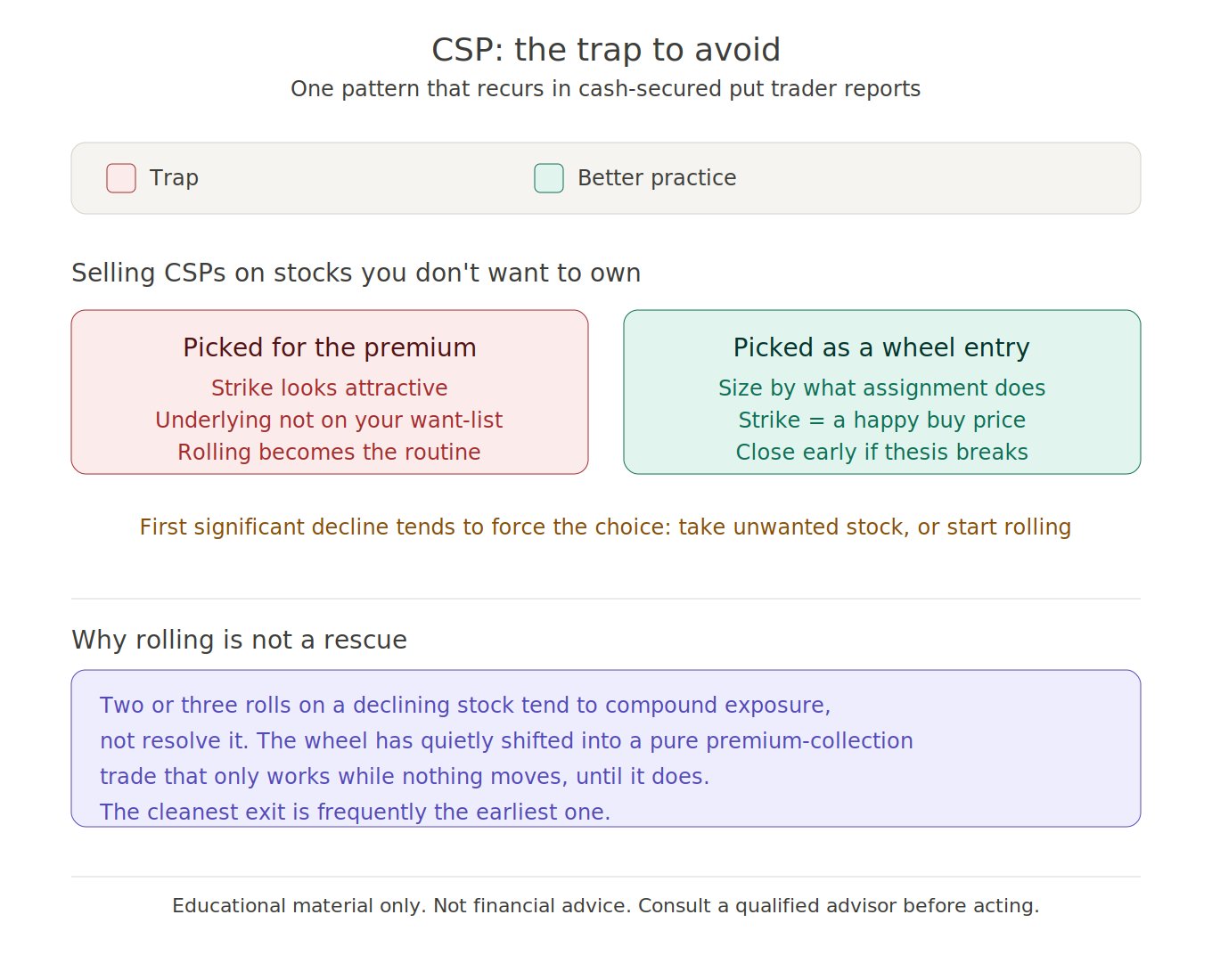

The trap to avoid

One pattern shows up in CSP trader reports more than any other. It does not look like a trap at the time. It looks like prudent management.

The wheel strategy works because assignment is an acceptable outcome at entry. When the strike was chosen for the premium rather than for the stock, the math is fine until the first significant decline — and then a choice gets forced: take unwanted shares, or start rolling. Rolling does not feel like a problem on the first attempt. It feels like a plan.

Two or three rolls into a declining stock and the position has quietly transformed. The wheel has shifted into a pure premium-collection trade that only works while nothing moves. The cash collateral is now committed to defending an entry the trader never really wanted. Each fresh credit looks attractive in isolation. The compounding capital exposure does not.

The cleaner approach: size CSP positions by what assignment would actually do to the portfolio, not by what the entry premium looks like. If the strike is not a buy price you would commit to on the underlying, the trade is wrong before it starts — no matter how good the premium looks today.

The 60-second summary

If the rest of the article disappeared and only one paragraph remained, it would be this: a cash-secured put is a wheel entry first and a premium trade second. Before reaching for the roll button, ask whether the strike still represents a buy price you would commit to on the underlying. If yes, holding into expiry or rolling once for a credit are both reasonable. If no, the cleanest exit is usually the earliest one — a defined, capped loss is preferable to a chain of rolls on a chart that is breaking down. Decide before the last week of the cycle, when delta and gamma still let you act on clean numbers. Wait until 5 DTE with the stock through the strike and a catalyst on the calendar, and the position is no longer a decision — the position is deciding for you.

Your CSP cycle, tracked end-to-end without the spreadsheet

MyOptionDiary tracks the cash-secured put through every step of its cycle — entry validation, the amber alert when the stock weakens past the threshold, four live roll scenarios when adjustment is on the table, automatic lot creation on assignment with the premium folded into your cost basis, and the next covered call written against the same lot. No CSV re-imports between steps. The decisions in this article are the same. The math is just already on the screen.

Disclaimer. MyOptionDiary is a trade recording journal — a personal record-keeping and educational tool. It is not a trading advisory, broker, financial advisor, or investment platform, and does not provide any form of financial advice or trading recommendations.

This article describes adjustment scenarios and practitioner patterns observed among options traders. It is educational material. Every position, account, and market condition is different; no single approach is universally correct. Outcomes described in worked examples are illustrative — actual results will vary.

Before making any adjustment to a live position, consider your own risk tolerance, capital, and tax situation, and consult a qualified financial advisor if you are uncertain. To the maximum extent permitted by law, MyOptionDiary and its author shall not be liable for any trading losses, financial losses, missed opportunities, tax consequences, or any direct, indirect, incidental, or consequential damages arising from your use of this article or reliance on any information, scenario, or pattern described herein. You are solely responsible for your own trading decisions and their outcomes.