How to Roll Covered Calls for Credit (and when not to)

Your covered call went through the strike. The roll choices on your screen all look ugly. Here is how experienced wheel traders think through the decision — and the two patterns that catch even careful ones.

If you found this article, the situation is probably specific. You sold a covered call a few weeks ago at a strike that felt safely out of the money. The stock has rallied. The call is now ITM, your buyback price has tripled, and the obvious roll choices all collect a thin credit, a real debit, or an awkward extension you did not plan for. The window for a comfortable adjustment has narrowed, and every session feels like it is making the math worse.

This is a position most wheel traders end up in eventually. There are four real options, not just rolling. Which one fits depends on whether you would actually mind being called away, how much extrinsic value is left in the call, and what the underlying is doing next. The math behind a "good roll" versus a "bad roll" is not complicated once the moving parts are visible. This article walks through the framework — Greeks, a worked NFLX example, the two trap setups worth knowing about, and a flowchart to anchor the decision.

What a covered call actually is

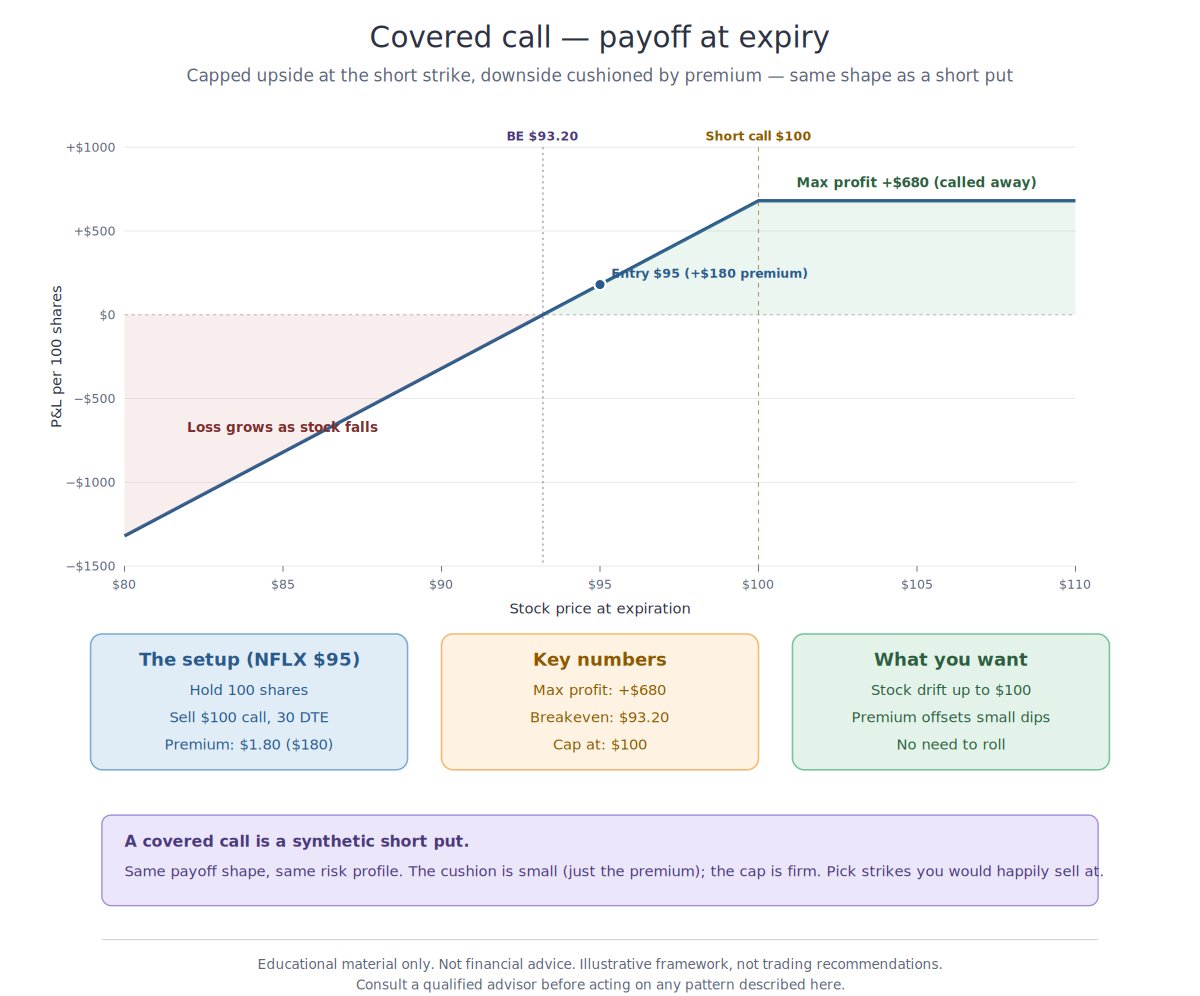

A covered call is a position where you own 100 shares and sell a call against them to collect premium. The premium is yours to keep no matter what happens. In exchange, you accept that if the stock closes above the strike at expiration, your shares get called away at that strike — you sell the shares, the cycle ends, and you start again.

The payoff at expiry has a specific shape: capped upside at the short strike, with the downside cushioned (just slightly) by the premium you collected at entry. It is mechanically the same shape as a short put — same risk profile, same payoff diagram, same considerations.

When the adjustment conversation typically starts

Two scenarios dominate. In the first, the stock has rallied hard and the short call is now in the money — assignment is likely at a price the trader may not love. In the second, the stock has dropped and the call is worth pennies, but the share position is underwater and the trader is considering ways to defend it without capping further upside.

Trigger signals

- Delta on the short call has moved from 0.20–0.35 at entry into the 0.45+ range. The market is now pricing ITM as the more likely outcome.

- DTE has dropped inside 21 with the stock near or through the strike. Gamma is accelerating — small moves in the underlying produce large, whippy changes in the call's price.

- The stock has rallied through the short strike and is still trending. Positions at this point have historically ended in assignment more often than not.

- The stock has dropped 8–10% or more since entry. The call is worthless, but the share position is bleeding.

- A known catalyst is approaching while the call is near the money. Earnings, ex-dividend dates, Fed meetings — early assignment risk spikes the day before ex-dividend on ITM calls.

The four real options

Most articles on this topic skip directly to "roll for credit" as if it were the only answer. It is not. There are four paths worth considering, and which one fits depends on the specifics of the position.

A — Let the shares get called away

When the strike sits above the original cost basis and the total return (premium plus share appreciation) is acceptable, some traders simply hold the position into expiry. Assignment in this situation is a designed outcome of the covered call strategy, not a loss. Historically one of the most underused options in the playbook — traders intuitively want to "do something," and accepting the cap feels passive. It is not. It is the trade working as planned.

B — Roll up and out for a credit

The current call is closed and a new call is opened at a higher strike and later expiry. One rule matters more than any other here: accept the trade only if it collects a net credit. Rolling for a net debit extends duration without compensation — paying to keep a losing position alive longer is rarely the right move. Act before 21 DTE if you can. After that, last-week gamma makes the buyback expensive and the credit gets thin or vanishes entirely.

C — Close the call, keep the shares

If the thesis has shifted and you now expect a much larger move up, you can close the call (accepting the realized loss) and hold the shares uncapped. This one is rare for a reason — it converts a defined-outcome position into a directional bet on the stock. Worth doing only when there is a specific reason to expect the next leg up. Not because the current setup feels frustrating.

D — Close the whole position

The shares are sold and the call is bought back simultaneously. This one is for situations where the stock thesis itself is broken — continuing to defend shares you no longer want to own generally compounds a prior decision rather than resolving it. The other case is when capital is needed elsewhere and this position is no longer the best use of it.

The Greeks behind the decision

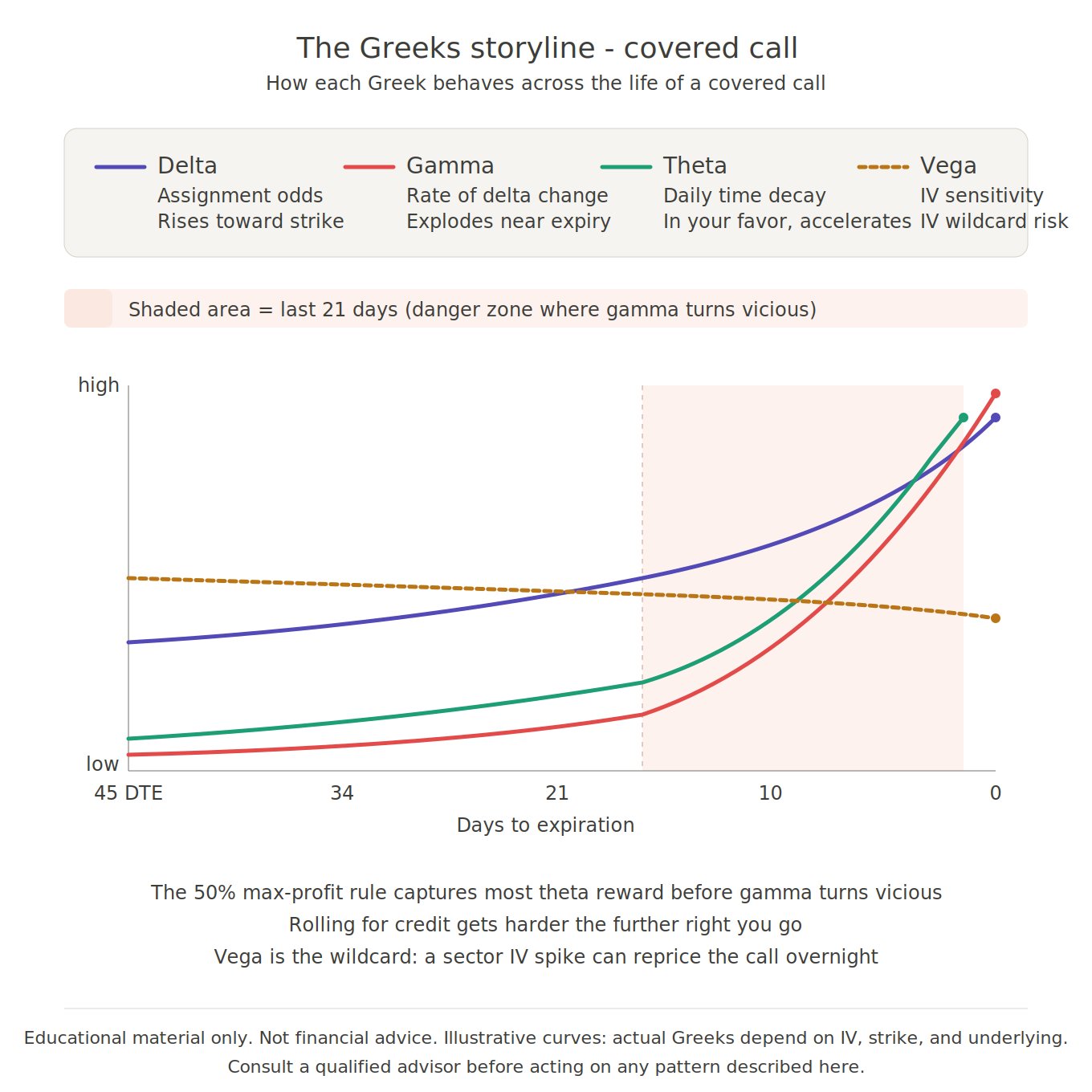

The four options above are the what. The Greeks explain the when — why the same position can be easy to manage at 35 DTE and nearly impossible at 7 DTE.

Delta — the storyline. Entry for a typical covered call is around 0.30 delta — roughly a 70% chance the call expires worthless. When delta climbs into the 0.45–0.60 range, the stock is demonstrating that the strike was too close to where it wants to trade. Past 0.70, the short call starts behaving almost like being short 100 shares of stock — every dollar the stock moves up hits the position nearly dollar-for-dollar. Of all the Greeks, this is the one to watch first when deciding whether to adjust.

Gamma — slow at the start, vicious at the end. At 45 DTE with the stock comfortably below the strike, gamma is small — delta changes slowly and the position is predictable session to session. The same call at 5 DTE with the stock pinned near the strike has gamma so high that delta can swing from 0.30 to 0.70 inside a single session. This is why the majority of covered call blow-ups historically happen inside the last week: the trader was fine on Friday, the stock rallies 3% on Monday, and the buyback cost has tripled by the open.

Theta — the paycheck, front-loaded to expiration. Theta is why the trade pays at all. It accrues in the position's favor every single day. But theta is not linear — the bulk of a 45-DTE call's time value decays in the final 21 days, and the final week accounts for the biggest daily numbers. The 50% max-profit early-close principle exists because it captures most of the theta reward while stepping aside before last-week gamma becomes difficult to manage. Closing early gives up the final few dollars of decay, but avoids the scenario where one bad session erases weeks of accumulated gain.

One covered-call-specific quirk applies to dividend-paying names: as DTE shortens on an ITM short call, extrinsic value drops toward zero, and if that remaining extrinsic falls below an upcoming dividend, the counterparty has an arbitrage incentive to exercise early. The shares get assigned at the strike the day before ex-dividend, and the seller forfeits both the dividend and any further upside. On dividend names, watching the short call's extrinsic value against upcoming ex-dividend dates is routine position management — not an optional refinement.

Vega — small, but running the wrong way. A short call position is short vega — rising IV raises the price of the call, which raises the cost to close the position, even if the stock has not moved. The common failure mode: a 30-delta call is sold on a quiet stock, nothing happens for two weeks, then earnings are announced on a peer company and sector IV spikes 8 points. The call is suddenly 25% more expensive to close. The math gets cleaner when you decide on adjustments before a known catalyst rather than during it.

The interaction that matters. When delta is rising through the strike, gamma is accelerating because DTE is short, AND vega is spiking because of an event — all at once — the short call's price moves faster than linear math would suggest. This is the "stuck" setup: rolling for a credit is no longer possible because the buyback has exploded, closing means a visible loss, and every session compounds the problem. The pattern is the same every time: the setup (delta rising + DTE under 21 + upcoming catalyst) is visible days before the explosion. The traders who get out cleanly tend to act on recognition, not reaction.

The Greeks in plain English

The five paragraphs above use the names traders give to five different ways a covered call can move — delta, gamma, theta, vega, and how they combine. In plainer terms:

Delta is the current odds the shares get called away. Low is typically desired (around 25–30% at entry), and 45% is where the position usually warrants a fresh look.

Gamma is how fast those odds change when the stock moves. Low and manageable early, aggressive in the last three weeks.

Theta is the daily income from time passing — which is why the trade pays at all. It speeds up near expiration, but so do the risks. The 50%-of-max-profit close is a common rule of thumb for that reason: take most of the reward, skip the messy part.

Vega is the penalty that appears when market-wide fear rises — earnings week, macro headlines — even when the underlying stock has not moved.

One covered-call-specific risk on dividend-paying stocks: a short call that is ITM and running low on extrinsic value just before an ex-dividend date can be assigned early. The shares get delivered at the strike, the dividend is forfeit, and any further upside is lost. Which is why checking the dividend calendar before selling covered calls on high-yield names is worth the 30 seconds it takes.

The "interaction" paragraph is describing a specific bad setup: the stock rallying into the strike AND being in the final three weeks AND a news event spiking fear, all at once. Most traders who learn to recognize that setup find it easier to exit before it fully arrives than to manage it afterward.

A worked example: NFLX

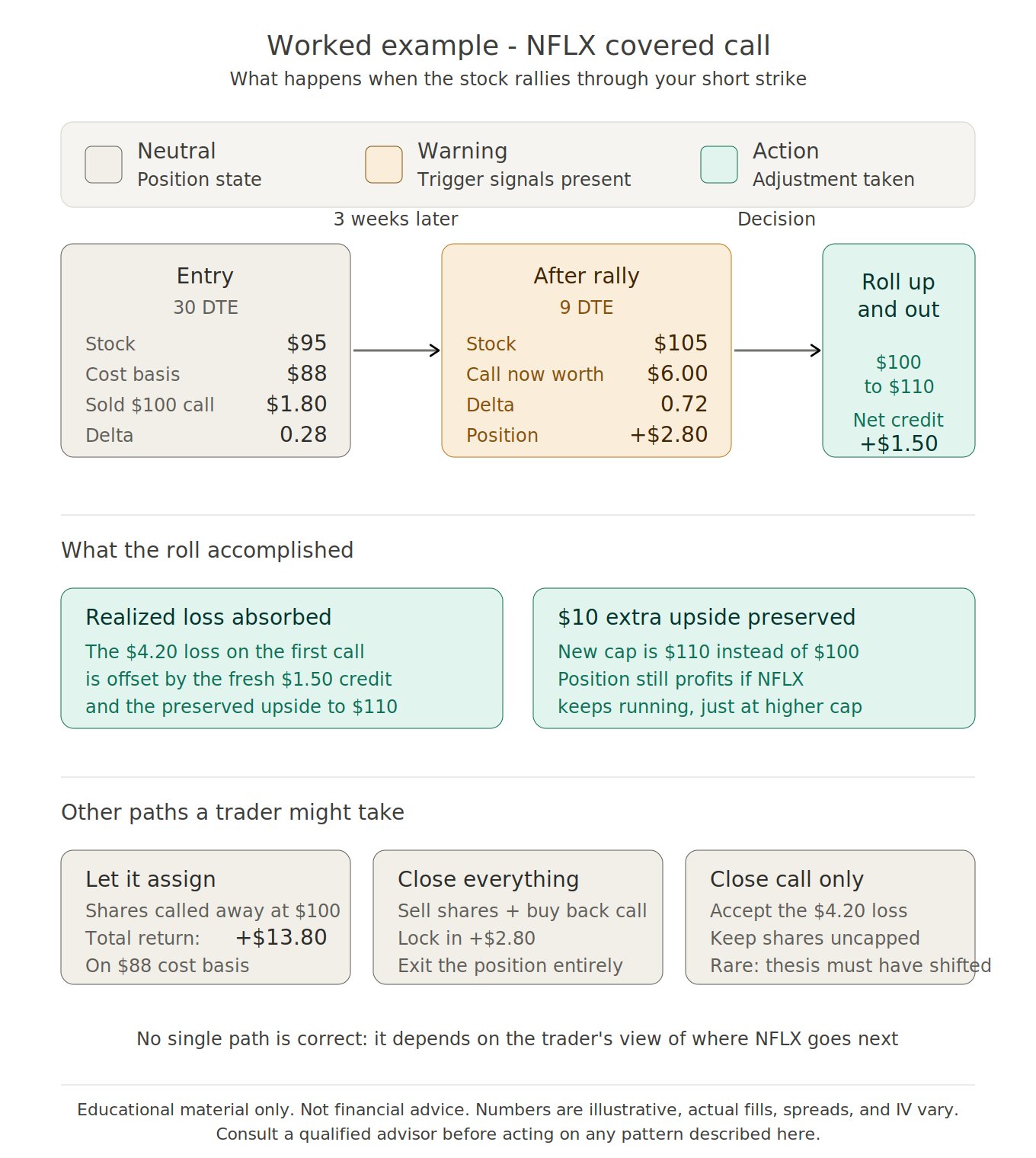

Setup. NFLX trading at $95. A trader owns 100 shares at cost $88. Sold the $100 call for $1.80 with 30 DTE. Entry delta approximately 0.28 — a textbook covered call entry.

What happened. Three weeks later NFLX is at $105. The short call is now worth $6.00, which represents a $4.20 unrealized loss on the call. Shares are up $7.00 from where the trade was opened. Net position unrealized: +$2.80 per share. Delta on the short call is 0.72 — deep ITM territory. DTE is 9.

One potential response. The $100 call was rolled out to $110 the following month for a $1.50 net credit. The realized loss on the first call was absorbed; the new credit was collected; $10 of additional upside (from $100 to $110) was preserved before the new cap would apply. If NFLX continued running past $110, the position would still be profitable — just capped at a better number.

This is one path among several. A trader who saw the thesis differently might have closed the position entirely at +$2.80 per share and moved on. A trader with strong conviction in further upside might have closed the call alone, accepted the $4.20 loss, and held the shares uncapped. A trader satisfied with the original setup might simply have let the shares get called away at $100 — which on the original $88 cost basis plus the $1.80 of premium works out to +$13.80 per share. Each of those is defensible. None of them is universally correct without context the chart cannot show.

A decision tree to anchor the choice

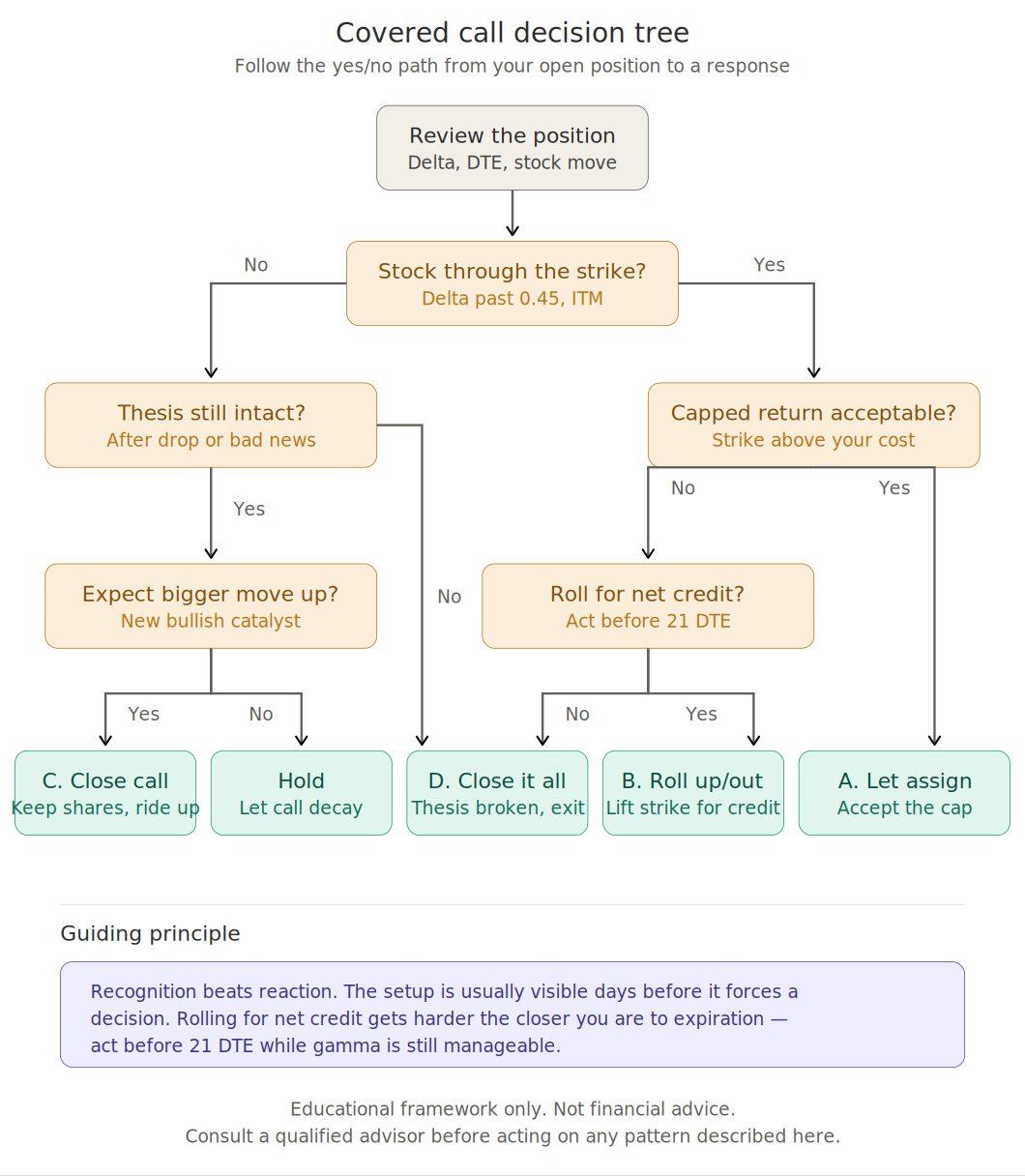

When the position is moving and the screen is asking for a decision, the actual question to answer is rarely "should I roll?" It is closer to: has the original thesis held? If yes, are you willing to be called away at the current strike? If no, the right action depends on whether you still want to own the shares at all. The flowchart below traces the questions in roughly the order they need to be asked.

The principle at the bottom of the chart is the one worth tattooing somewhere: recognition beats reaction. The setup that ends in a panicked Friday roll is usually visible days earlier — the delta climbing, the DTE shrinking, the catalyst on the calendar. Acting on the recognition while the math is still clean is dramatically easier than managing the same position once the buyback has tripled.

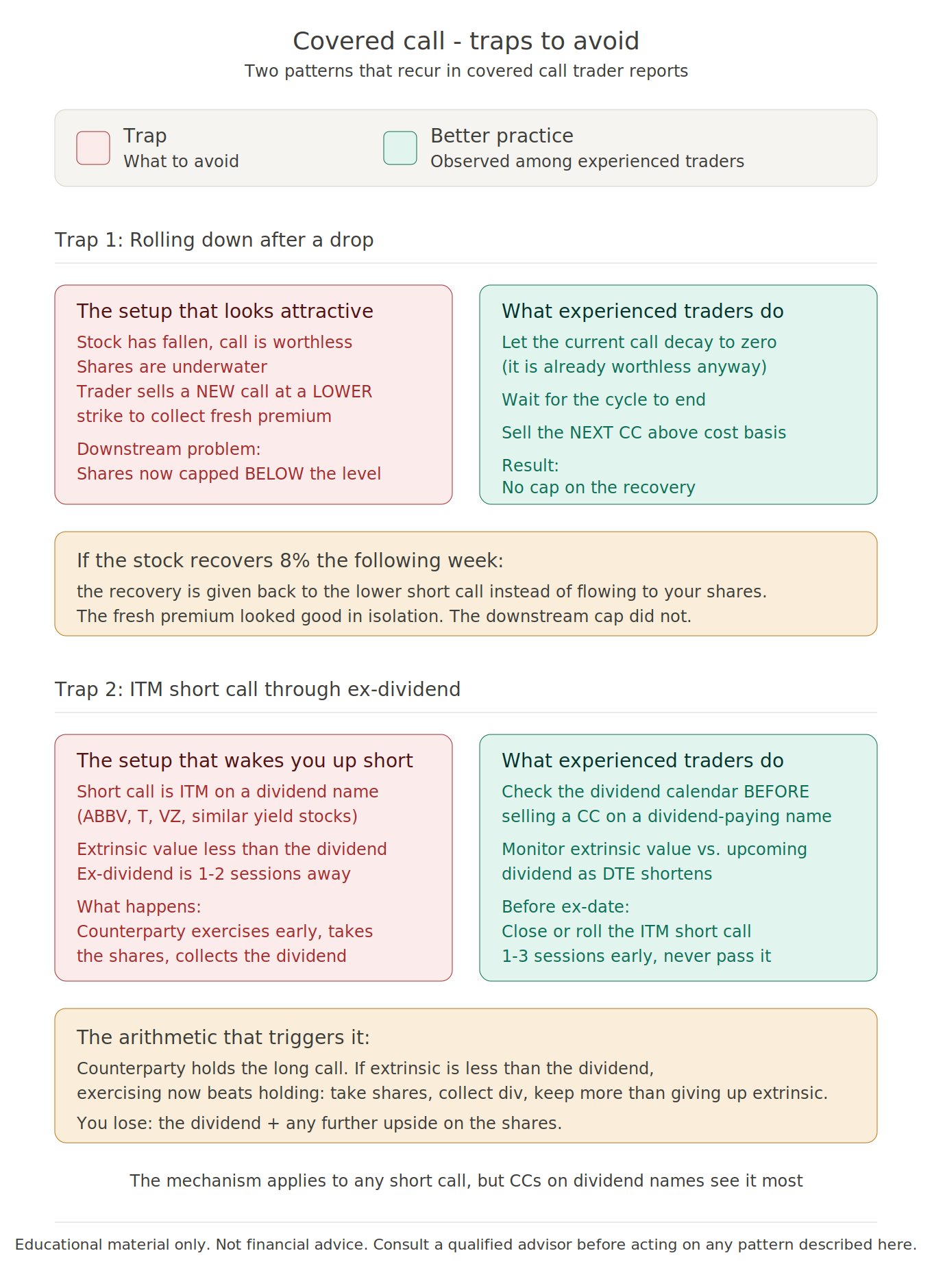

Two traps to avoid

Both of these patterns show up often enough to call out specifically. The visual below summarises both — the prose beneath it adds the part the visual cannot, which is why each one is so easy to walk into.

This one is seductive because the new premium is real cash collected today. The cost is the cap you just installed below the level the shares need to recover to. Stock bounces 8% the next week and that bounce flows to the short call, not to you.

The cleaner play when the thesis is still intact: let the existing call decay toward zero (it is already worthless) and sell the next covered call above cost basis on the next cycle.

When an ITM short call has less extrinsic value remaining than the upcoming dividend, the counterparty has an arbitrage: exercise, take the shares, collect the dividend, pocket the difference. You wake up assigned the day before ex-date, minus the dividend and any further upside.

Most common on dividend names — ABBV, T, VZ, similar yield stocks. The fix is mechanical: check the dividend calendar before opening the trade, and close or roll any ITM short call one to three sessions before ex-date rather than holding through it.

The 60-second summary

If the rest of the article disappeared and only one paragraph remained, it would be this: rolling a covered call works in some situations, not all. Before reaching for the roll, ask whether the thesis has held, whether assignment at the current strike would actually be a bad outcome, and whether the math of the proposed roll collects a real credit at a strike worth defending. Decide before the last week of the cycle, when delta and gamma still let you act on clean numbers. If you wait until 5 DTE with the stock past the strike and a catalyst on the calendar, the roll is no longer the decision — the position is already deciding for you.

When the alert fires, the math is already done

MyOptionDiary is the desktop wheel-strategy journal I built because I got tired of opening the option chain to do roll math under time pressure. When a covered call alert fires, four roll scenarios appear inline — close, +30 days, +45 days, and roll up for a strike improvement — each with live net credit, new delta, new breakeven, and combined P&L computed against the actual chain. The decision below is the same one this article describes. The numbers are just already on the screen.

Disclaimer. MyOptionDiary is a trade recording journal — a personal record-keeping and educational tool. It is not a trading advisory, broker, financial advisor, or investment platform, and does not provide any form of financial advice or trading recommendations.

This article describes adjustment scenarios and practitioner patterns observed among experienced options traders. It is educational material. Every position, account, and market condition is different; no single approach is universally correct. Outcomes described in worked examples are illustrative — actual results will vary.

Before making any adjustment to a live position, consider your own risk tolerance, capital, and tax situation, and consult a qualified financial advisor if you are uncertain. To the maximum extent permitted by law, MyOptionDiary and its author shall not be liable for any trading losses, financial losses, missed opportunities, tax consequences, or any direct, indirect, incidental, or consequential damages arising from your use of this article or reliance on any information, scenario, or pattern described herein. You are solely responsible for your own trading decisions and their outcomes.