How to Adjust an Iron Butterfly (and why the body stays locked)

Five adjustment paths, the structural reason the ATM body never moves, and why an Iron Butterfly is managed earlier and tighter than its wider-strike cousin.

What an Iron Butterfly is

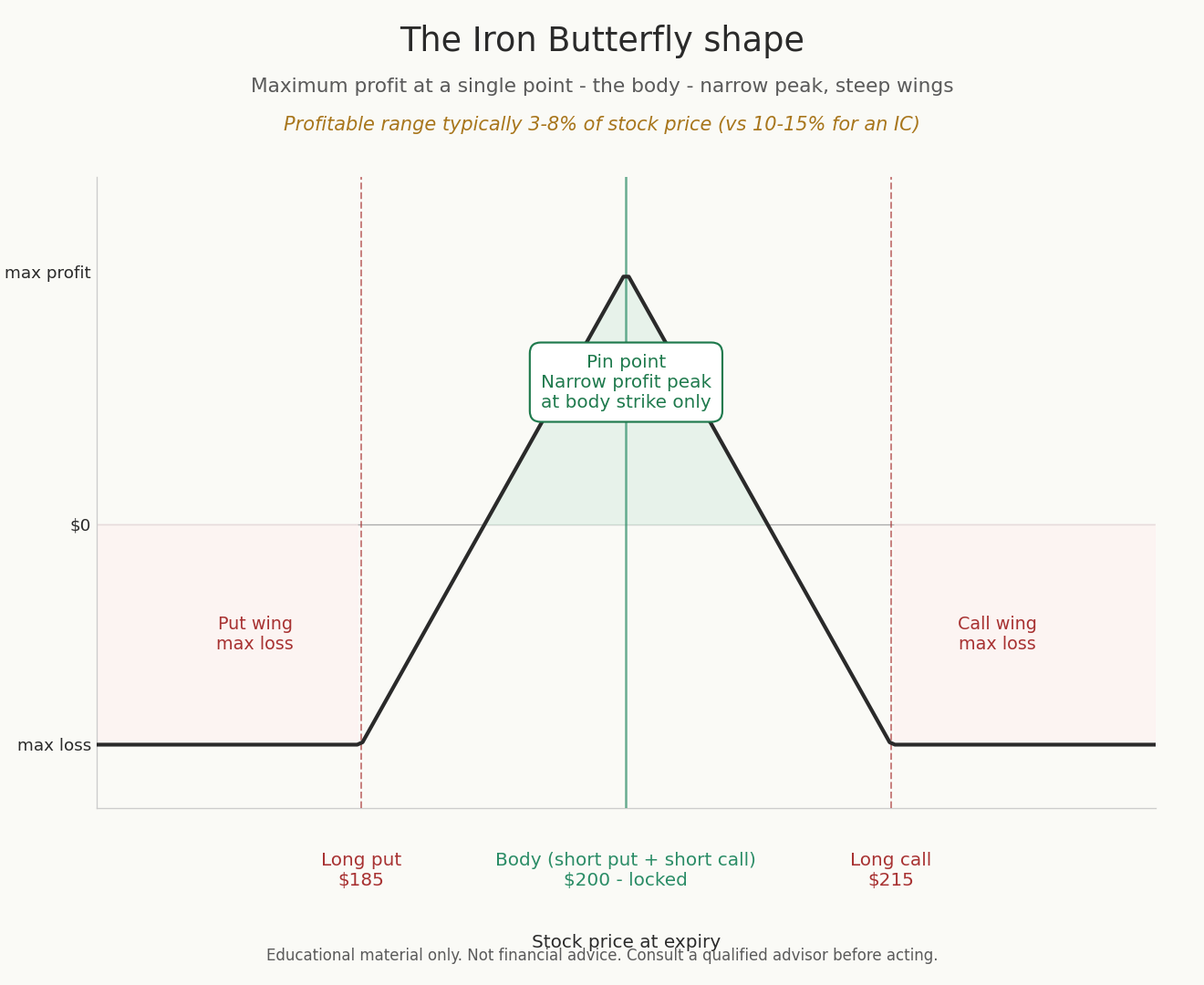

An Iron Butterfly (IB) is a four-leg position that sells a put and a call at the same ATM strike (the body) while buying a lower-strike put and a higher-strike call as wings. A net credit is collected up front. The position profits when the stock pins near the body at expiry, producing a tent-shaped payoff.

The structure collects significantly more premium than an equivalent OTM Iron Condor because both spreads are sold ATM. The trade-off is a much narrower profitable range — roughly 3–8% of the stock price — and both wings are closer to being tested at all times.

When the adjustment conversation starts

The stock has drifted meaningfully away from the ATM body and is approaching or breaching one of the wing strikes. Because the body is at-the-money from the outset, IB positions rarely sit "quiet" for long; the adjustment conversation begins sooner and more often than on an Iron Condor. The tested wing is now producing a loss while the untested wing decays toward its maximum value.

Trigger signals

- The stock has moved 2–4% away from the body in either direction. Because the profitable range on an IB is narrow, even modest moves test the structure quickly.

- Delta on the tested short leg has moved from roughly 0.50 at entry into the 0.55–0.65 range. This is the band where the adjustment conversation most commonly begins — earlier in the range when DTE is under 21 or IV is expanding, later when DTE is still long and IV is stable. Since the short strikes were ATM to begin with, the absolute numbers matter less than the direction and speed of change.

- The position's unrealized loss has reached 1× to 2× the initial credit received. On an IB this matters even more than on an IC because premium is higher and losses develop faster. At roughly 1× the credit, adjustment is actively considered; at 2× the credit, closing is the more common choice over further defense.

- The stock has closed past one of the wing buy strikes. Maximum loss on that side is realized at the mark; further adverse movement is capped, but the position is locked into the loss at expiry without an adjustment.

- DTE has dropped inside 21 with the stock displaced from the body. Gamma on both wings is already elevated because both short strikes were ATM at entry, and the last three weeks accelerate that exposure further.

- A scheduled catalyst (earnings, macro event) is approaching. IBs sold into compressed IV ahead of an event face the risk that a large post-event move breaches a wing — one of the hardest IB outcomes to defend.

- A scheduled ex-dividend date is approaching on a dividend-paying underlying while the short call leg (the body) is ITM or very close to ITM, and the call's remaining extrinsic value is less than the dividend amount. This is a clean early-assignment setup specific to the call-side of the body — the short put leg of the body does not carry this asymmetry.

Why the body stays locked

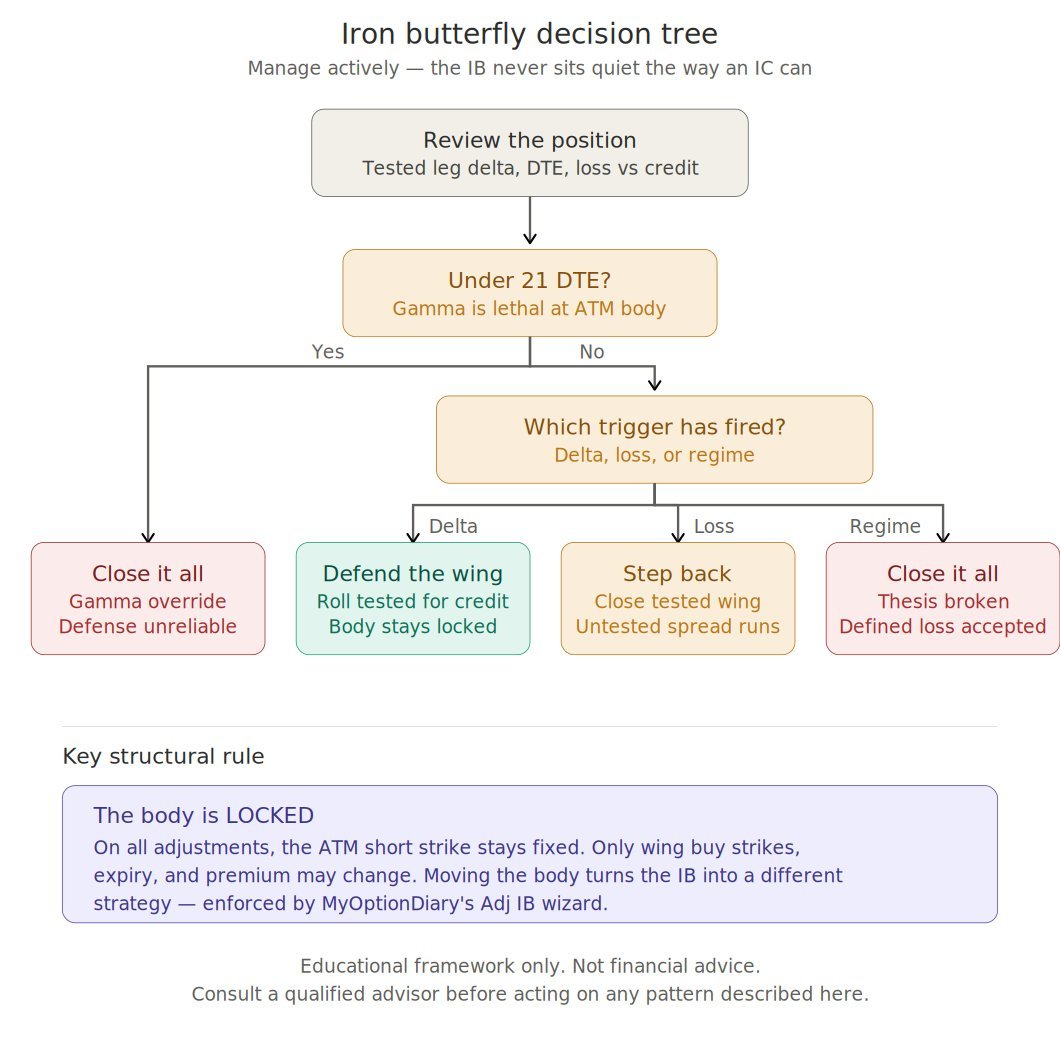

On every Iron Butterfly adjustment in MyOptionDiary's Adj IB wizard, the ATM body — the shared short strike — is locked. Only the wing buy strikes, the expiry, and the premium can change on any roll or partial close. Moving the body would fundamentally change the position from an Iron Butterfly into a different strategy.

This constraint reflects how experienced IB traders manage the structure. The body is the entire identity of the trade; if it moves, the trade is no longer a butterfly but a re-entered IC at new strikes. The wizard enforces this separation explicitly so adjustments stay inside the IB structure rather than quietly drifting into a different strategy.

Five adjustment options on the table

A — Roll the tested wing for a credit

The threatened wing (put wing on downside tests, call wing on upside tests) is closed and reopened at a wider buy strike on a later expiry. The body stays locked at the original ATM strike. The untested wing remains in place. The roll works cleanest when it produces a net credit — rolling for a debit extends duration without compensation.

This is the most common defensive response on an IB. The credit received offsets some of the realized loss on the tested side, the wider wing buys cushion against further adverse movement, and the later expiry restores theta to the position.

B — Widen the tested wing without changing expiry

The long option on the tested side is sold back and replaced with a further-OTM long on the same expiry. The maximum loss on that wing increases, but the short leg retains more extrinsic value and the break-even shifts. The body stays at the original ATM strike.

Uncommon in practice — most IB traders prefer rolling the wing out (Option A), which achieves similar defensive intent more cleanly. This option is used when the trader believes the current move may pause but not reverse and wants to avoid extending duration.

C — Reduce size on the tested wing

A portion of the contracts on the tested wing is bought back to reduce directional exposure. The body and the untested wing stay untouched. Commonly used when the move appears extended and a reversal is plausible but not certain.

Requires a multi-contract IB to be practical — on a single-contract position there is no size to reduce, only to close. The proportion bought back is a trader judgment — heavier reductions when conviction in the original thesis has weakened, lighter reductions when the move appears to be a pause rather than a reversal.

D — Close the tested wing entirely

The full tested spread (both short and long) is closed, locking in the realized loss on that side. What remains is the untested credit spread — a bear call spread on the upside-tested case, or a bull put spread on the downside-tested case.

Reserved for situations where the tested move is viewed as continuing rather than reverting, and a one-sided credit spread is acceptable exposure. The remaining single-spread position is no longer an IB but a directional credit play on the side that has held.

E — Close the whole position

All four legs are closed simultaneously. The defined loss is accepted, buying power is freed, and the trade is exited.

This path is chosen when the stock has moved decisively beyond the wing strike, when the thesis (sideways pin near the body) is broken, or when the running loss is approaching 1.5–2.5× the initial credit. IB losses develop faster than IC losses, so some traders use the lower end of that range — closing at 1.5× credit rather than waiting for 2×.

The story of the Greeks

Delta — high from the start, nets only briefly

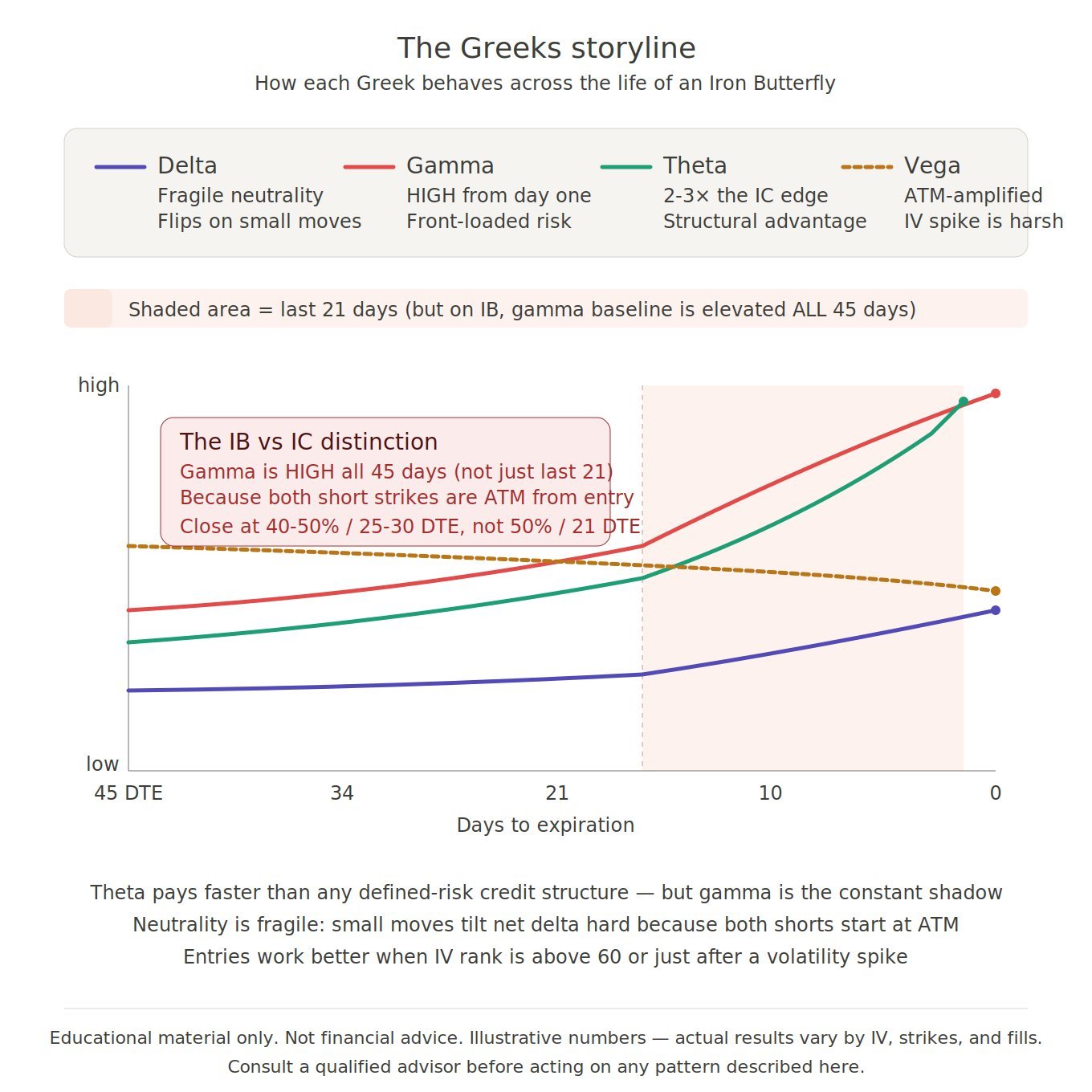

At entry, the two short legs are both at the ATM body strike — the short call contributes roughly −0.50 delta, the short put contributes roughly +0.50 delta, and they cancel almost perfectly. This makes the initial position delta-neutral, but the neutrality is fragile.

A small stock move away from the body causes the tested wing's delta to dominate quickly because both short strikes are already at-the-money. This is the structural difference from an IC: an IB spends its entire life with both short legs close to the money, and net delta flips hard on relatively small moves.

Gamma — elevated from entry, not just near expiration

An IC's gamma is low at entry because both short legs are wide OTM. An IB's gamma is elevated from day one because both short legs are ATM. Small stock moves produce larger delta changes earlier in the trade than they would on an IC at equivalent DTE.

The gamma acceleration in the final 21 days is still real, but the baseline is higher throughout. This is why the IB position is managed more actively and closed earlier than an equivalent IC — the tail risk is front-loaded into the position's entire life, not concentrated at the end.

Theta — the highest of any defined-risk credit structure

Because both spreads are sold at the body rather than OTM, the premium collected on an IB is two to three times the equivalent-width IC on the same underlying. The position pays faster per day than any OTM-based credit structure. Theta accelerates in the last 21 days the same way other short-premium positions do, and peaks in the final week.

The 50% of max credit early-close rule of thumb applies strongly here — pushing for the final theta on an IB exposes the trade to the sharpest gamma risk of any common strategy, because both short strikes are sitting ATM the whole time.

One dividend-related concern is amplified on IBs versus ICs: because the short call leg is at the ATM body rather than OTM, any meaningful rally in the underlying pushes the short call ITM quickly. On a dividend-paying underlying, this turns into a meaningful early-assignment risk well before expiration. On dividend names, the dividend calendar is checked at entry, and the position is closed or actively managed around any ex-dividend date within the life of the trade rather than held passively.

Vega — short on both wings, amplified by ATM positioning

An IB is net short vega. Rising IV after entry raises the price on BOTH wings simultaneously, the same as on an IC. The IB-specific twist: because both short strikes are ATM, vega per unit of IV change is higher on an IB than on an equivalent IC. A 5-point IV expansion that costs an IC a moderate mark-to-market hit costs an IB a larger one.

Conversely, IV compression after entry produces a faster favorable P&L swing on an IB than on an IC — the structural reason IB entries are preferred when IV rank is above 60 or just after a volatility spike.

The worst setup for an IB is a meaningful directional move in the underlying while IV is expanding AND DTE is under 21. All three Greeks turn against the position simultaneously, and because both short strikes started ATM, the starting exposure is already higher than an IC at the same DTE.

A position that opened at a 4% expected-move implied range can breach a wing on a single 6% session move when that session also coincides with an IV spike. The refinement that applies here is tighter than the IC's 0.25 delta threshold: on an IB, the adjustment conversation begins when the tested short leg delta moves past 0.55 in combination with rising IV, rather than waiting for the 0.60–0.65 zone.

If this is newer to you

The Iron Butterfly, without the jargon

An Iron Butterfly is the high-risk, high-premium cousin of the Iron Condor. The sweet spot where it makes maximum profit is a very narrow band right at the starting stock price, which means even small stock moves put pressure on the position. Because both short strikes are right at-the-money from the start, the position is always close to being tested — it never sits quiet the way an IC can for weeks.

Delta on the tested wing climbs fast when the stock moves. Gamma is elevated from day one, not just near expiration. Theta pays faster than almost any other defined-risk trade, which is the reason to use the structure at all. Vega works against the position when market fear rises, and the pain is amplified because both strikes sit at-the-money.

The interaction paragraph above describes the pile-on: the stock moves, IV spikes, and DTE is short — all at once. The IB structure is closed much earlier than an IC would be, often at 40–50% of max credit captured rather than pushing toward expiration.

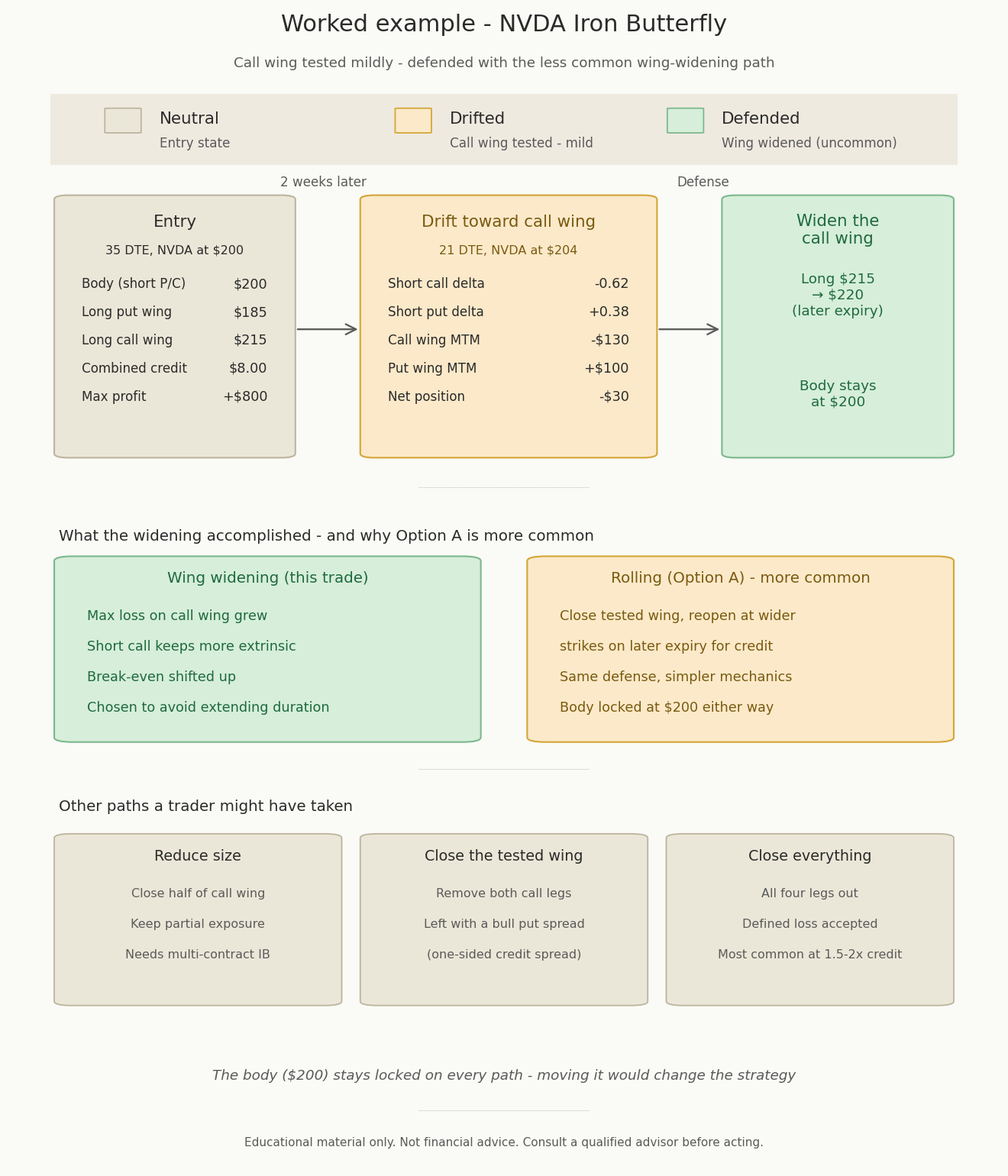

Worked example — NVDA Iron Butterfly

Setup

NVDA is trading $200. A trader sells a $200 put and $200 call at the ATM body, and buys a $185 put and $215 call as the wings. Net credit $8.00 per share, $800 on one contract pair. 35 DTE. Entry delta on the short call is −0.50, on the short put is +0.50; net delta near zero. Max profit $800 if NVDA pins at $200. Max loss per wing is ($15 wide − $8.00 credit) × 100 = $700.

What happened

Two weeks later NVDA has drifted to $204. 21 DTE remaining. The short call delta has moved from −0.50 at entry to roughly −0.62 — the call wing is the tested side. The short put has drifted to approximately +0.38. Call-wing mark-to-market loss is approximately $130; put-wing unrealized gain is approximately $100. Net position is running at roughly a $30 mark-to-market loss on the $800 maximum — still defendable, but the adjustment conversation has started.

One potential response

This particular trader chose the less common wing-widening path (Option B) rather than the more typical roll (Option A), because they wanted to avoid extending duration. Because the Adj IB wizard locks the body at $200, the strikes that can change on any roll are the wing long legs — the short strikes at $200 remain fixed for the life of the IB structure.

The call wing was widened: the long call at $215 was sold and replaced with a long call at $220 on a later expiry, and the short $200 call was rolled to the same later expiry at the same $200 strike. The put wing was left untouched. Net transaction: a modest debit was paid for the wing widening, but the extended duration restored theta to the position and the wider wing gave the short $200 call more extrinsic value to work with. The body remained at $200, preserving the IB structure.

One path among several. A trader using the more common approach would have rolled the tested wing out entirely (Option A) for a credit. A trader who viewed the drift as the start of a larger move might have reduced size on the call wing (Option C) instead, closed the tested wing entirely (Option D — converting the remainder to a one-sided credit spread), or closed the whole position (Option E) and redeployed capital elsewhere.

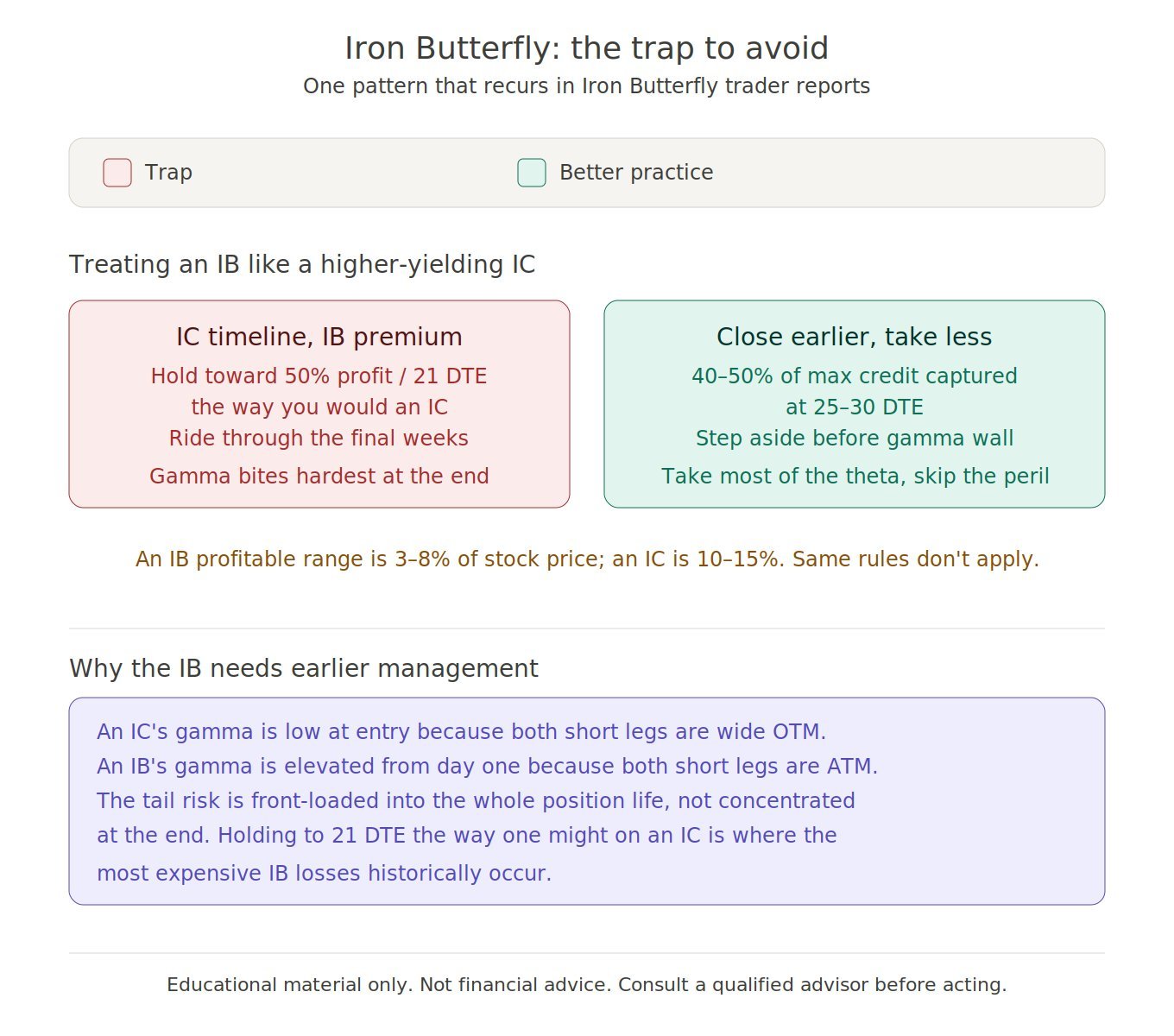

The trap to avoid

A pattern that recurs in trader reports: treating an Iron Butterfly as a "higher-yielding Iron Condor" and managing it on the same timeframe. The structural difference is meaningful — an IB's gamma exposure is elevated from entry, not just near expiration, and its profitable range is roughly 3–8% of the stock price rather than the 10–15% of a well-spaced IC. Holding an IB into the final two weeks the way one might hold an IC is where the most expensive IB losses occur.

A more frequent practice on IBs: closing at 40–50% of max credit captured and at 25–30 DTE, rather than pushing toward the 21 DTE threshold that works on OTM-based structures. The premium captured is smaller in absolute terms, but the realized win rate over many cycles is higher because the gamma wall is sidestepped before it does the most damage.

Iron Butterflies with the body locked on every adjustment

MyOptionDiary supports the full Iron Butterfly adjustment chain through the Adj IB wizard — roll the tested wing, widen, reduce size, close the tested wing, close the position. The ATM body is locked on every adjustment so the structure stays an IB rather than quietly drifting into a different strategy. Each adjustment is recorded as part of the trade chain, with net credit/debit, max profit, max loss per wing, and remaining open legs tracked automatically. The 21 DTE gamma window and tested-leg delta are surfaced as alerts before the trade enters the danger zone. The decisions in this article are the same. The math is just already on the screen.

MyOptionDiary is a trade recording journal — a personal record-keeping and educational tool. It is not a trading advisory, broker, financial advisor, or investment platform, and does not provide any form of financial advice or trading recommendations.

This guide describes adjustment scenarios and patterns drawn from active options trading. Every position, account, and market condition is different; no single approach is universally correct. Outcomes described in worked examples are illustrative — actual results will vary.

Before making any adjustment to a live position, consider your own risk tolerance, capital, and tax situation, and consult a qualified financial advisor if you are uncertain. To the maximum extent permitted by law, MyOptionDiary and its author shall not be liable for any trading losses, financial losses, missed opportunities, tax consequences, or any direct, indirect, incidental, or consequential damages arising from your use of this guide. You are solely responsible for your own trading decisions and their outcomes.