How to Adjust a Calendar Spread: a five-path defense playbook

A practitioner walk-through of the full adjustment space on the rare debit structure where time works for the trader, why the value builds in the last 10–14 days, and the high-IV entry trap that flips the structural advantage into a structural drag.

What a Calendar Spread is

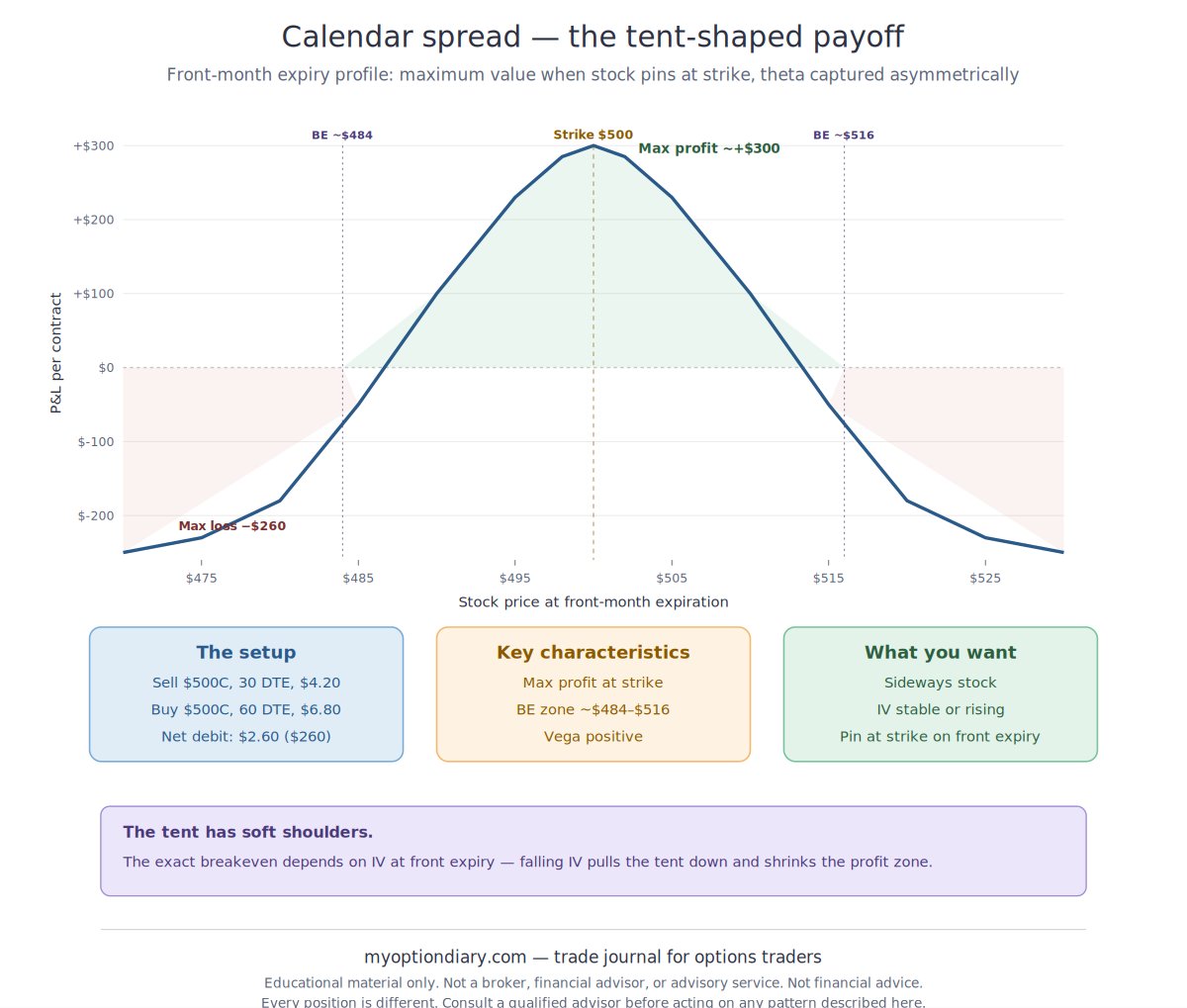

A Calendar Spread is a two-leg position that sells a near-term option (the front-month, short leg) and buys a longer-dated option at the same strike (the back-month, long leg). Both legs are the same type — both calls or both puts. A net debit is paid up front: the back-month costs more than the front-month brings in.

The position profits when the underlying stays near the strike as the front-month approaches expiration. The short leg decays faster than the long leg, and the trader pockets the difference. The structure is unusual among common strategies in being net long vega and net long theta at the same time — time decay and IV expansion both tend to work in the position's favor, inside the profitable range around the strike.

The payoff is tent-shaped, not flat-and-capped like a vertical spread. Maximum profit sits directly at the strike on the day the front-month expires; the breakeven shoulders sit a few percent on either side. The shoulders are "soft" — they move based on what IV looks like at front-month expiration, not just the underlying's closing price.

When the adjustment conversation typically starts

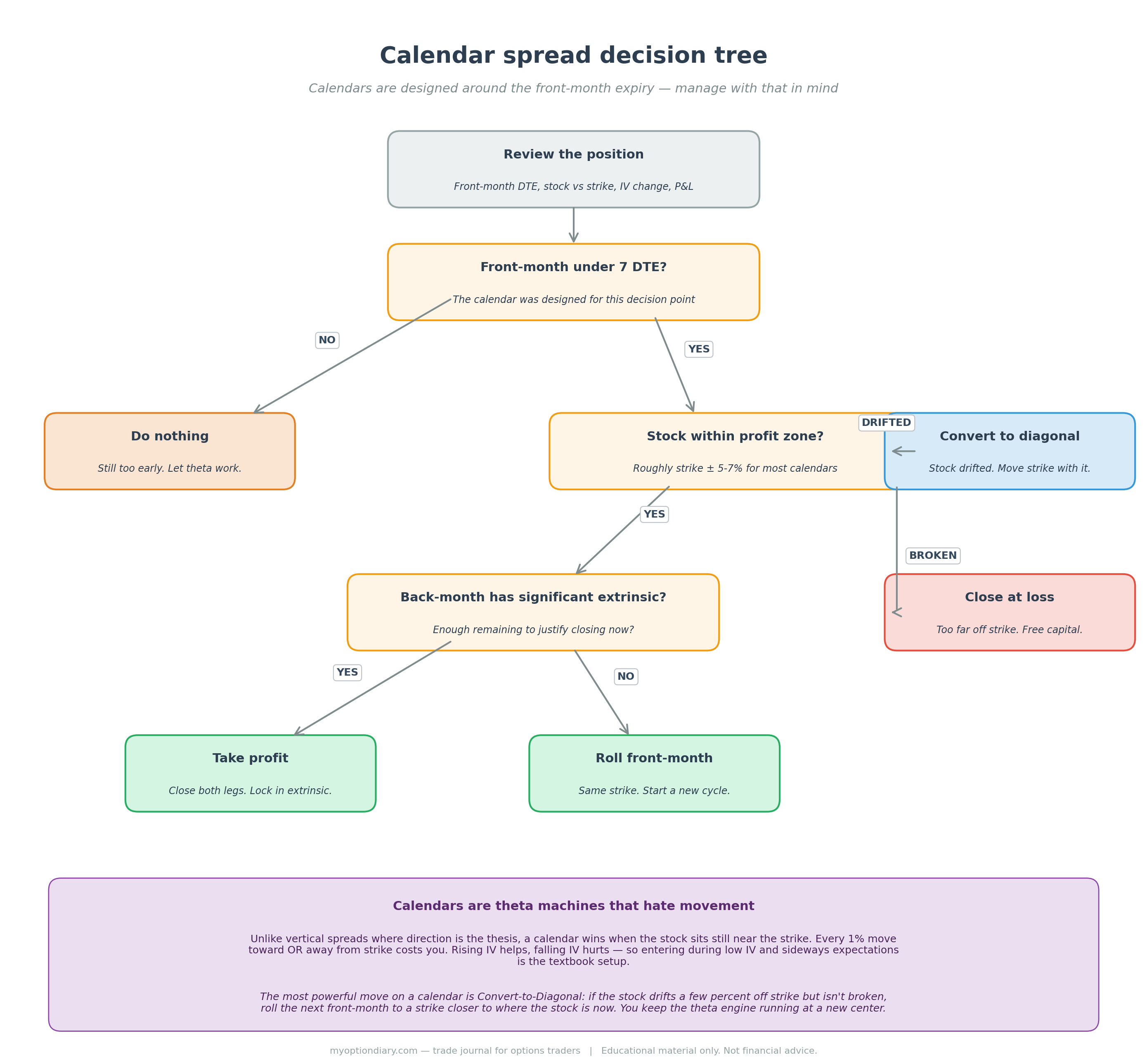

Calendars run on a life cycle rather than an open-ended duration. The primary adjustment moment arrives as the front-month nears expiration: the short leg has either done its job (decayed toward zero with the underlying near the strike) or been rendered untenable (the underlying has moved far from the strike). A second moment arrives mid-cycle when the underlying drifts meaningfully away from the strike — the position's profit potential erodes, and the conversation shifts to whether to reposition or exit. A third moment arrives when IV behavior diverges from the entry thesis.

Trigger signals

- The front-month short leg is within 7–10 days of expiration and the underlying is near the strike. The position is approaching maximum profit, and the adjustment decision is whether to close the whole calendar or roll the short leg forward to begin a new theta-collection cycle against the back-month anchor.

- The underlying has moved more than 5–7% away from the strike in either direction during the life of the front-month. Both legs have lost value, and the position's path toward profit has been disrupted.

- IV on the underlying has compressed materially since entry. The back-month leg has shed value disproportionately (it carries more vega than the front-month), and the position shows an unrealized loss even with the underlying near the strike.

- A scheduled catalyst — earnings, macro event — is approaching. The decision becomes whether to close before the event to lock in pre-event IV expansion, or hold through it and accept the post-event IV crush.

- The underlying has moved so far from the strike that the front-month short leg is deep ITM or deep OTM. At either extreme, the short leg's extrinsic value has collapsed and the calendar's profit potential is exhausted for this cycle.

Five adjustment paths on the table

The MyOptionDiary Adj Cal wizard supports five primary paths. They appear here in the order the decision tree presents them, from continuing the structure (when working) to exiting it (when broken).

A — Roll the front-month forward

The front-month short leg is bought to close, and a new short leg is sold at the same strike on the next expiration cycle. The back-month long leg stays in place as the anchor. This is the signature Calendar adjustment and the primary income-generation mechanism. Each short-leg cycle that expires worthless or near-worthless adds to the cumulative chain P&L while the back-month continues to accrue toward its own expiry. The roll tends to be taken only when the new short leg collects a meaningful credit — if the underlying has drifted such that the next cycle's premium is thin, the better path is often to step aside rather than extend an unprofitable structure.

B — Take profit (close both legs)

Both legs are closed simultaneously and the realized gain is locked in. This path comes up when the underlying has pinned at the strike, the front-month has decayed to near-zero, and the back-month still carries meaningful extrinsic value. The lockout point in trader reports often sits around 80–100% of debit returned: the front-month is essentially done its work, and continuing to hold for the last few percent exposes the back-month to gamma and vega risk that the early cycle already paid the trader for.

C — Convert to diagonal (roll the front-month to a different strike)

The front-month short leg is bought to close, and a new short leg is sold on the next expiration cycle — but at a different strike than the original, typically closer to where the underlying has now drifted. This formally converts the Calendar into a Diagonal. The path comes up when the underlying has moved meaningfully away from the original strike and continuing to sell short legs at the original strike no longer produces useful premium. The back-month anchor stays in place; only the short-leg strike shifts. The wizard names this move "Widen to Diagonal."

D — Close at a loss

Both legs are closed and a capped loss is realized. The path comes up when the underlying has moved so far from the strike that neither continuing the structure nor restructuring it makes sense. It also fires when the IV expansion the trade was positioned for has failed to materialize, or when the back-month has lost enough value to the IV compression that the remaining upside no longer justifies the capital tied up.

E — Doing nothing

The maximum loss on a calendar is already defined and capped at the original debit paid. When the front-month still has meaningful time remaining, the underlying is inside the profitable zone, and the thesis remains intact, holding the position is a valid response on its own. The practitioner playbook names "do nothing" as a path of its own — a reminder that the option exists, since traders tend to over-manage when it isn't on the list. The Calendar-specific reason this matters: the position's value builds back-loaded, in the final 10–14 days as the front-month extrinsic collapses. A calendar that looks underwater mid-cycle often finishes near maximum profit if the underlying stays near the strike.

The Story of the Greeks

The Greeks on a Calendar move differently than on any other structure in this series. The position is long the longer-dated back-month and short the nearer-dated front-month, with both legs at the same strike. Same-strike, different-expiration is what produces the unusual combination — net long theta on a debit spread, net long vega without giving up theta, and net short gamma when the underlying sits near the strike.

Delta — near zero at entry, the drift signal

A calendar sold with the strike at-the-money carries net delta close to zero at entry. The short front-month and long back-month have similar delta magnitudes that offset. Net delta shifts as the underlying moves away from the strike, because the two legs have different rates of delta change. The shorter-dated leg reacts more sharply to underlying moves than the longer-dated leg.

On a call calendar with the underlying rising: the short leg's delta climbs faster than the long leg's, so net delta becomes negative and the position suffers. On a call calendar with the underlying falling: the short leg's delta drops faster than the long leg's, so net delta becomes positive — and the position suffers in the other direction. Delta on a calendar functions as the drift signal, not the direction signal. When net delta moves materially away from zero, the underlying has moved out of the position's profitable zone.

Gamma — net short, the drift accelerator

Calendars are net short gamma when the underlying sits near the strike. The front-month leg carries more gamma than the back-month because gamma amplifies as time-to-expiration shrinks. The net effect: as the underlying drifts away from the strike, the position's delta moves against the trader at an accelerating pace rather than a cushioned one. A small drift compounds before the trader can react.

This is why calendar exit thresholds tend to be defined as underlying price bands around the strike (commonly ±5% of the strike) rather than as percentages-of-max or DTE rules — the gamma-driven acceleration on drift makes the underlying-price band the more useful trigger.

Theta — the paycheck, on a debit spread

This is the feature that makes calendars distinctive: a debit spread with positive net theta. The short front-month decays faster than the long back-month because the exponential decay curve accelerates as expiration approaches. A 30-day option loses value faster per day than a 90-day option at the same strike and IV. The trader effectively sells near-term decay and buys far-term decay, pocketing the difference each day the underlying sits near the strike.

Theta is strongest when the underlying is near the strike (where the short leg has the most extrinsic to decay) and weakens as the underlying moves away. Unlike Bull Call Spreads or Bear Put Spreads, holding a calendar through sideways action is the plan — time working in the position's favor is the primary profit mechanism.

Vega — net long, often the main reason to use the structure

Calendars are net long vega. The back-month carries more vega than the front-month because vega scales with time-to-expiration, so rising IV after entry helps the position significantly and falling IV hurts it. This vega positioning is the second reason calendars get used alongside theta: they express a view that IV will expand on a specific underlying, even without a directional view on the price.

The failure mode that recurs in trader reports on the vega side: a calendar gets entered before an anticipated catalyst — earnings, macro event — expecting IV to expand into it. IV does expand as anticipated. But the post-event IV crush is typically larger than the pre-event expansion, and the back-month gets hit harder than the front-month because the back-month has more vega to lose. The position ends up worse than it was the day before the catalyst, even when the IV pattern played out exactly as predicted. A pattern that recurs among calendar traders who entered specifically for an IV-expansion thesis: the position is closed one or two trading sessions before the catalyst, capturing the pre-event rise without the post-event crush.

The dangerous setup for a calendar is the underlying moving meaningfully away from the strike while IV is also compressing. Delta and gamma both work against the position as the underlying drifts, and vega compounds the damage because the back-month's vega loss exceeds the front-month's vega gain.

A calendar paid $4.60 at entry can be marked at $2.00 or lower after a 7% underlying move combined with 5 points of IV compression — a severe unrealized loss from a combination that, taken individually, would not be catastrophic. The "profitable range" framing that recurs in calendar trader reports is roughly ±3–5% of the underlying price at entry. Outside that range, the structural advantages reverse, and the position tends to be exited rather than defended.

If this is newer to you

The Greeks story, without the jargon

The four sections above use technical names for four distinct ways a Calendar Spread can move. Translated: a calendar is a bet that a stock will stay near a chosen price long enough for a near-dated option to decay into near-worthlessness while a longer-dated option at the same strike retains value. The trade is paid for up front (net debit), but unlike other debit spreads, time works in the trader's favor. This is the signature feature.

Delta on a calendar is near zero at entry if the strike is chosen at the current price, and it signals trouble when the stock starts drifting away from the strike. Gamma means that trouble accelerates — a small drift compounds because the near-dated leg reacts faster than the far-dated leg.

Theta is the income being collected, strongest when the stock sits near the strike. Vega helps the position when IV on the underlying rises, which makes calendars a common vehicle for expressing a view that IV will expand on a particular stock around an upcoming event. The interaction callout above describes the calendar's worst case: the stock moves meaningfully away from the strike and IV compresses at the same time, compounding losses from multiple directions. Calendar traders tend to define a profitable range at entry (commonly ±5% of the strike) and close the position when the stock leaves that range, rather than waiting for front-month expiry.

Worked example — SPY Calendar Spread

Setup

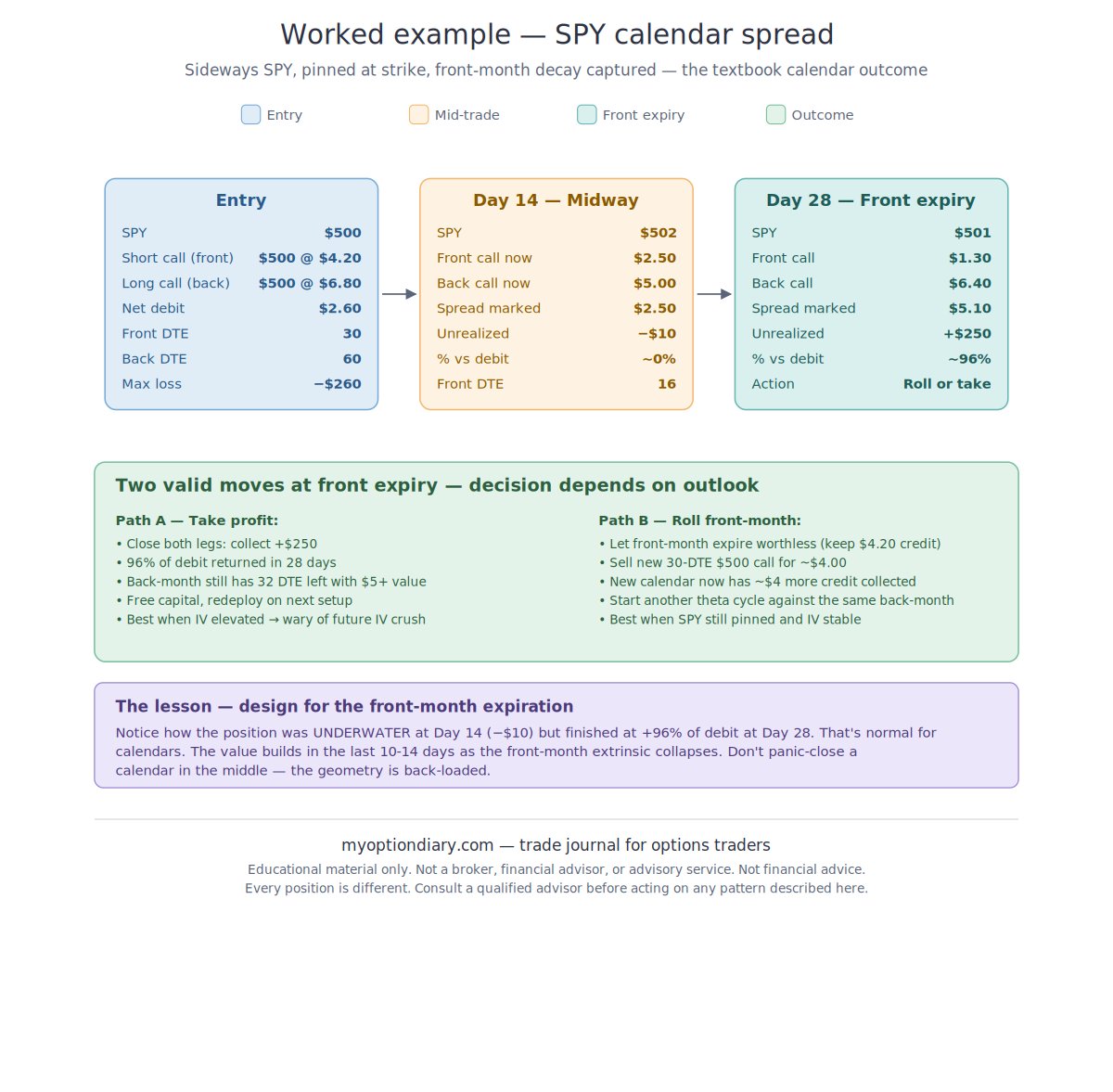

SPY is trading $500. A trader sells the $500 call (30 DTE) for $4.20 and buys the $500 call (60 DTE) for $6.80 on the same strike. Net debit: $6.80 − $4.20 = $2.60 per spread, $260 on 1 contract. Max loss: $260 (the debit paid). The trade is positioned for SPY to stay near $500 through the front-month's 30-day life cycle.

What happened

By day 14 (midway through the front-month), SPY has drifted to $502. The front $500 call has decayed from $4.20 to $2.50; the back $500 call has decayed from $6.80 to $5.00. The spread is marked at $2.50 combined — an unrealized loss of $10 against the $2.60 debit, roughly 0% of debit recovered. 16 DTE remain on the front-month.

By day 28 (front-month expiration approaching), SPY sits at $501. The front $500 call is marked at $1.30 (mostly extrinsic, near expiry); the back $500 call is marked at $6.40 (still 32 DTE remaining and holding most of its value). The spread is now marked at $5.10 combined — an unrealized gain of $250 against the $2.60 debit. 96% of the debit has been returned in 28 days.

Two paths at front-month expiration

The textbook two-way decision at this point:

Take profit. Both legs are closed and the +$250 gain is locked in. The back-month still has 32 days remaining and at least $5+ of value, so closing now still captures most of what the calendar can offer. The freed capital redeploys into the next setup. This path comes up when IV looked elevated at entry and there's a concern about future IV compression — locking in the gain is the conservative choice.

Roll the front-month. The front-month expires worthless (keeping the $4.20 credit originally received) and a new 30-DTE $500 call is sold for ~$4.00 of fresh credit. The same back-month anchor now produces a second theta-collection cycle. This path comes up when SPY still looks likely to pin near $500 and IV looks stable.

The decision is not "which is right" — both paths have a real case. The choice depends on whether the next 30 days are expected to behave like the last 30 days, and on how the trader values free capital versus an extended theta-collection chain. The MyOptionDiary Adj Cal wizard supports both paths and records each as a step in the chain so the cumulative P&L is tracked end-to-end.

The calendar was underwater at day 14 (−$10) but finished at +$250 by day 28. That pattern is normal. The position's value builds in the final 10–14 days as the front-month extrinsic collapses faster and faster, while the back-month's extrinsic continues to grind down at its slower far-dated pace. A calendar that looks like it isn't working at the halfway point often finishes near maximum profit if the underlying stays near the strike. The temptation to panic-close in the middle is generally the wrong instinct on this structure — the geometry is back-loaded by design.

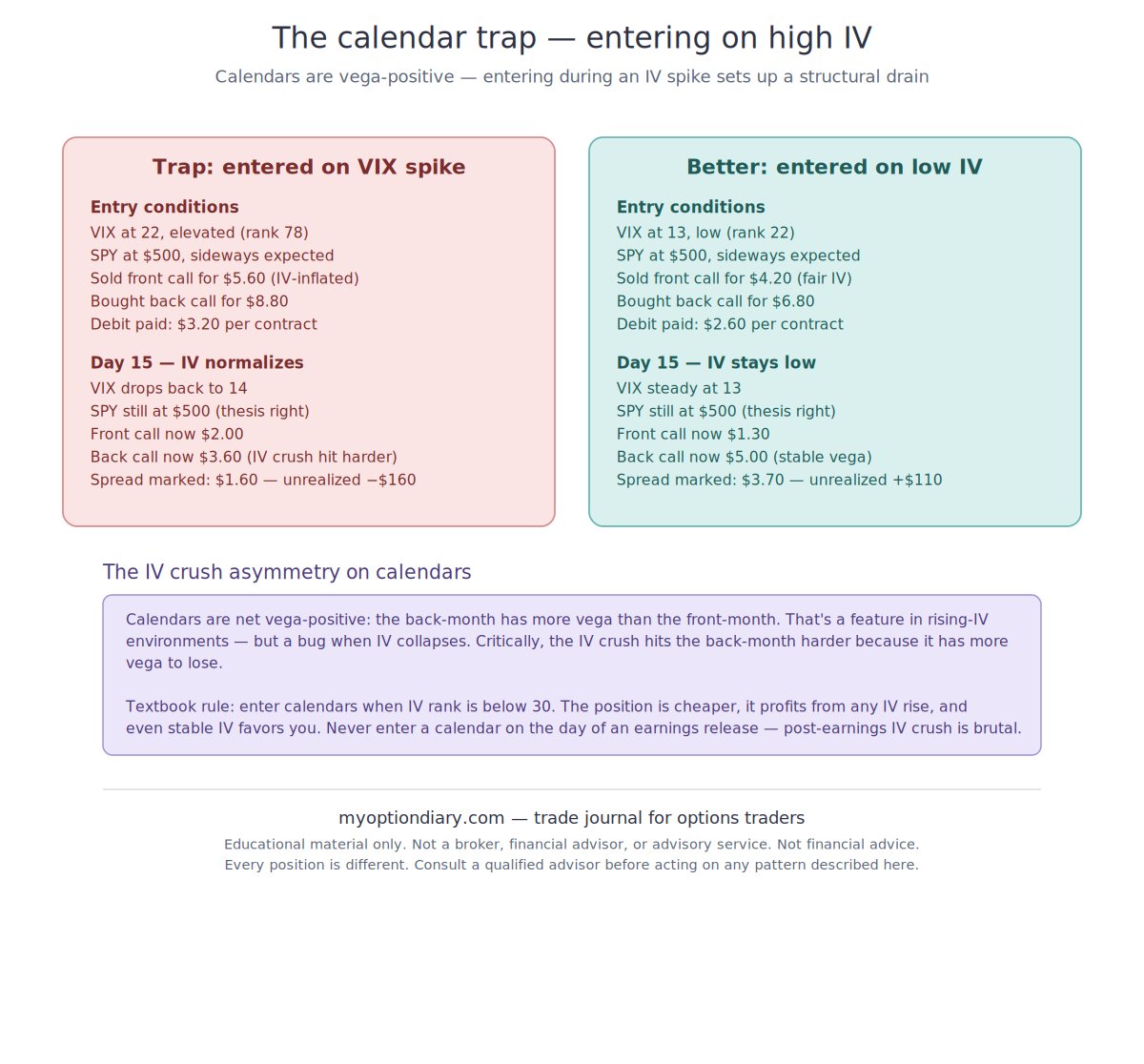

The trap to avoid

A pattern that recurs in calendar trader reports: entering a Calendar Spread during an elevated-IV regime, on the reasoning that "calendars are long vega, so high IV should help." The reasoning is half right and half backwards. Calendars are long vega — but the more meaningful question is which way IV is going to move from here, not where it sits today.

The same SPY $500 calendar described above looks materially different at two different entry points. With VIX at 22 and IV elevated (rank 78), the front $500 call sells for $5.60 and the back $500 call costs $8.80 — debit paid is $3.20. With VIX at 13 and IV low (rank 22), the front sells for $4.20 and the back costs $6.80 — debit paid is $2.60. Same underlying, same strikes, same DTE structure, materially different entry economics.

Now look at what happens 15 days later if SPY sits still at $500 (the thesis is right) but IV normalizes. On the high-IV entry: VIX drops back to 14, front call now at $2.00, back call at $3.60, spread marked at $1.60 — an unrealized loss of $160 even though the underlying did exactly what was predicted. On the low-IV entry: VIX stays at 13, front at $1.30, back at $5.00, spread marked at $3.70 — an unrealized gain of $110 with the same underlying behavior.

The asymmetry comes from where vega sits. The back-month carries more vega than the front-month, so when IV compresses, the back-month leg loses more value than the front-month gains back through its own IV compression. Net effect: the position's long-vega exposure works against the trader on the IV-normalization side of an elevated-IV entry, and works for the trader on the IV-expansion side of a low-IV entry. The rule that recurs in calendar playbooks: entries tend to behave better when IV rank is below roughly 30, where the asymmetric vega is positioned to help rather than hurt.

The trap has a specific failure mode around earnings. A calendar entered the day before earnings — even with the thesis "IV will expand into the print" — frequently ends up worse the day after, regardless of direction. Pre-event IV expansion is usually priced in by the day before the print; the post-event IV crush tends to be significantly larger than the pre-event rise; and the back-month gets hit harder than the front-month because of the vega differential. Calendars held through earnings have historically been among the least consistent debit-spread trades, regardless of how accurately the trader read the directional move.

Calendar Spreads with the full adjustment chain on screen

MyOptionDiary supports all five Calendar adjustment paths through the Adj Cal wizard — roll the front-month, take profit, convert to diagonal, close at loss, or pass. Each adjustment links back to the original entry as one continuous chain. Debit paid, current MTM, cumulative credits from rolled short legs, and net P&L across the chain update automatically. The ±5% drift band, the back-month extrinsic, and the IV-rank entry gate are surfaced as alerts. The decisions described here are the same. The math is already on the screen.

MyOptionDiary is a trade recording journal — a personal record-keeping and educational tool. It is not a trading advisory, broker, financial advisor, or investment platform, and does not provide any form of financial advice or trading recommendations.

This guide describes adjustment scenarios and patterns observed among experienced options traders. It is educational material. Every position, account, and market condition is different; no single approach is universally correct. Outcomes described in worked examples are illustrative — actual results will vary.

Before making any adjustment to a live position, consider your own risk tolerance, capital, and tax situation, and consult a qualified financial advisor if you are uncertain. To the maximum extent permitted by law, MyOptionDiary and its author shall not be liable for any trading losses, financial losses, missed opportunities, tax consequences, or any direct, indirect, incidental, or consequential damages arising from your use of this guide. You are solely responsible for your own trading decisions and their outcomes.